Business

BOI to start servicing Afreximbank’s EUR 2bn Debt After 1 year

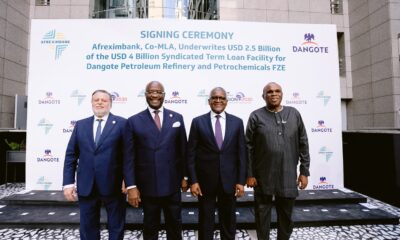

The Afreximbank’s EUR 2 billion syndicated term loan facility for Bank of Industry (BOI) Nigeria has a three-year tenor with quarterly repayments commencing after the first year.

In a statement, Afreximbank, said that it acted as one of the Initial Mandated Lead Arrangers, Bookrunner and Facility Agent in the said loan facility.

“Said the statement: The facility is backed by a first demand guarantee and is structured into two tranches.

Tranche A is guaranteed 85% by the Africa Finance Corporation and 15% by the Central Bank of Nigeria (CBN) for both principal and interest.

Tranche B is 100% guaranteed by the AFC for both principal and interest. The Bank disbursed its participation amount of EUR 175 million in September 2024 in two tranches of EUR 115 million in Tranche A and EUR 60 million under Tranche B.

Afreximbank was also involved in the processes leading to financial close and disbursement of up to EUR 2 billion by all the lenders, including the early bird syndication in August 2024 as the Facility Agent.

BOI is expected to use the proceeds of the facility to finance trade and trade related projects of eligible corporates in Nigeria.

“This significant transaction underscores Afreximbank’s commitment to supporting Nigeria’s economic growth,” said Mr. Denys Denya, Senior Executive Vice President at Afreximbank.

“By actively participating as lender, bookrunner, and agent, we are not only providing crucial financing to Bank of Industry but also facilitating access to critical resources that will empower Nigerian businesses and drive sustainable development across the country.

” Dr. Olasupo Olusi, Managing Director of Bank of Industry, stated: “This landmark syndicated facility of up to EUR 2 billion is a testament to the confidence global financial institutions have in the Bank of Industry’s track record and its pivotal role in driving Nigeria’s industrial and economic transformation.

We are particularly grateful for Afreximbank’s significant participation and unwavering support both as a lender and facilitator in this transaction.

This funding will empower us to further finance critical projects, ultimately fostering sustainable growth and development for corporates across Nigeria.”

Business

Royal African Society marks 125 years of Africa – Britain Businesses

The anniversary featured the Closing of Markets Ceremony and ringing of the exchange’s closing bell, alongside high-level sector discussions, fireside chats, the presentation of philanthropy awards and the unveiling of the Top African Brands in the UK and Top British Brands in Africa.

• Arunma Oteh, Chairperson of the Royal African Society

The Royal African Society has marked 125 years anniversary of Africa and Britain businesses and investments at a ceremony held at the London Stock Exchange.

The Wednesday event brought together the Emir of Kano, Muhammadu Sanusi II; President and Chief Executive Officer of Africa Finance Corporation, Samaila Zubairu; Chief Executive Officer of British International Investment, Leslie Maasdorp; Founder and Chief Executive Officer of Flutterwave, Olugbenga “GB” Agboola; Director and Chief Executive Officer of the Royal African Society, Stella Okotete; and other business, diplomatic and policy leaders.

Chairperson of the Royal African Society, Arunma Oteh, said that the organisation had spent 125 years fostering partnerships between both regions.

Oteh said that the celebration was aimed at deepening collaboration between Africa and the UK while promoting investment, innovation and shared prosperity.

The anniversary featured the Closing of Markets Ceremony and ringing of the exchange’s closing bell, alongside high-level sector discussions, fireside chats, the presentation of philanthropy awards and the unveiling of the Top African Brands in the UK and Top British Brands in Africa.

Business

US subjects imports from Nigeria to 12.5% tariff

The tariff affects imports from 60 economies that Washington says have not “imposed and effectively enforced a prohibition on the importation of goods produced with forced labour.”

The United States has imposed a 12.5 per cent tariff on imports from Nigeria as part of a new trade measure targeting countries it says have failed to prohibit the importation of goods produced with forced labour.

The tariff affects imports from 60 economies that Washington says have not “imposed and effectively enforced a prohibition on the importation of goods produced with forced labour.”

The measure was announced in a statement posted on the website of the Office of the United States Trade Representative on Thursday.

Nigeria is among the countries subject to the 12.5 per cent tariff, while India, Indonesia, Malaysia, Mexico and the United Kingdom will face a lower 10 per cent rate after adopting or committing to implement bans on imports linked to forced labour.

The move follows investigations launched by the USTR in May 2026 into 60 of the United States’ largest trading partners under Section 301 of the Trade Act.

According to the agency, it received more than 1,600 written submissions, held public hearings involving over 100 witnesses, and consulted more than 45 governments before announcing the tariffs.

Business

MTN Nigeria asks customers to trade old SIM packs for prizes

MTN named eight collection centres across the country where customers can deposit their items. The locations cover Lagos, Abuja, Kano, Jos, Delta, Port Harcourt, and Ibadan.

MTN Nigeria has invited customers to bring in old SIM packs, recharge cards, booster cards, dongles, and MTN-branded phones in exchange for prizes.

The telecom giant is running the campaign the under the hashtag #YelloMoments.

MTN launched the campaign on Wednesday, July 23, via its official social media pages, telling followers that items kept in drawers over the years could be worth something.

Customers who participate will also be featured on what MTN described as a “Memory Wall.”

Collection centres across Nigeria

MTN named eight collection centres across the country where customers can deposit their items. The locations cover Lagos, Abuja, Kano, Jos, Delta, Port Harcourt, and Ibadan.

In Lagos, customers can visit MTN Plaza at No. 1 Awolowo Road, Falomo, Ikoyi, or the office at 43 Allen Avenue, Ikeja. In Abuja, the collection point is at No. 4, Medeira Street, Maitama.

In Kano, it is at 2, Civil Centre Road. In Jos, Plateau State, the centre is at Plot 3119, Royalfield Road.

In Asaba, Delta State, the location is KLM 129, Benin–Asaba Expressway. In Port Harcourt, Rivers State, customers can go to 234, Old Aba Expressway, Opposite Hannah Fast Food.

In Ibadan, Oyo State, the drop-off point is at MTN Regional Office 1, Olubadan Avenue and Up/Zartech Road, Oluyole Estate.

Security Forces Rescue 9, Neutralise Terrorist in Kwara

Nigeria’s Enang Presents Credentials to German President Steinmeier (Images)

Zamfara LG Chairman Abduction: Security operatives intensify rescue efforts

Tech Expert, Zuckerberg trains with UFC champions, Adesanya, Alexander

Organ Trafficking: Ekweremadu bags 10 years in UK prison

SAINT OBI: Between his marriage and his death

-

Business3 days ago

Business3 days agoNaira Exchange Rates Thursday, 23 July

-

Sports3 days ago

Sports3 days agoNigeria’s NSC Chiefs Lead Team to 2026 Commonwealth Games in Glasgow

-

Politics3 days ago

Politics3 days agoFashola declares, “I’m not interested in becoming President of Nigeria”

-

News2 days ago

News2 days ago311 lawmakers say “YES!” to establish state police

-

Politics3 days ago

Politics3 days agoTimi Frank says Trump’s letter not political ‘endorsement’ of Tinubu

-

Business2 days ago

Business2 days agoNaira Exchange Rates Across Black Market, CBN, Commercial Banks Friday, July 24

-

News2 days ago

News2 days agoSoludo’s daughter bags First Class from UK university

-

News2 days ago

News2 days agoEleven poets jostle for $100,000, ‘Nigeria Prize for Literature 2026’