News

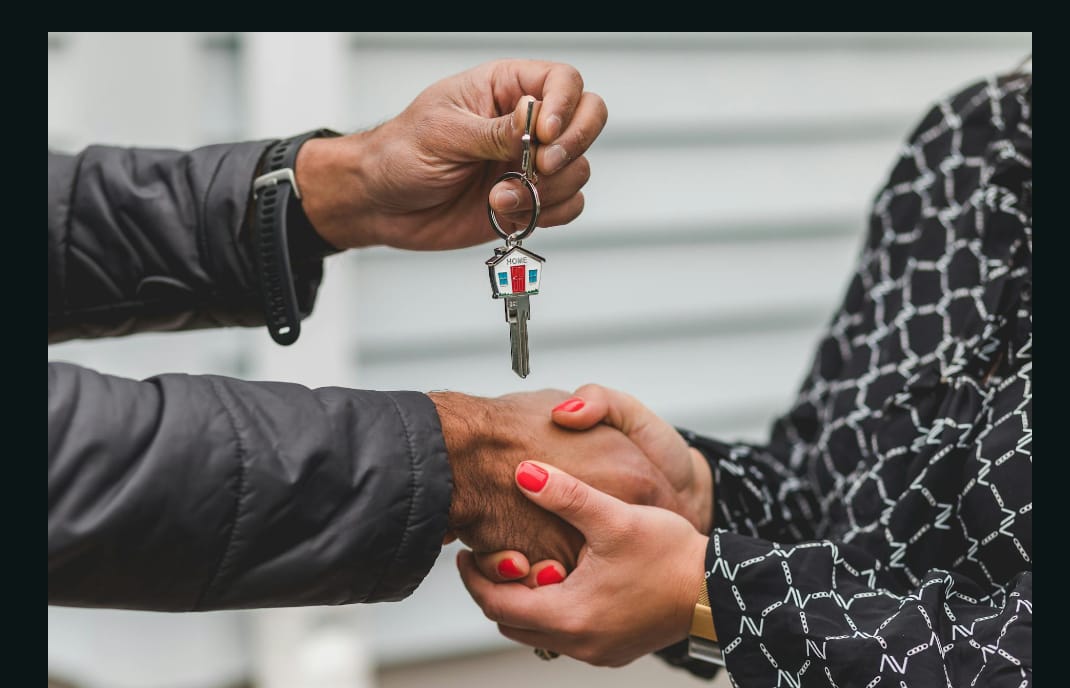

Understanding Mortgage Options in Nigeria’s Real Estate Market by Dennis Isong

For Nigerians considering a mortgage, thorough research and preparation are essential.

As more Nigerians aspire to become homeowners, understanding the available mortgage options becomes essential.

This article discusses mortgage financing in Nigeria, exploring the various options available to prospective homeowners and investors..

The Nigerian MortgageNigeria’s mortgage industry, while still developing, has made considerable strides in recent years.

The Federal Mortgage Bank of Nigeria (FMBN) and the Nigeria Mortgage Refinance Company (NMRC) play pivotal roles in shaping the mortgage sector.

These institutions work alongside commercial banks and primary mortgage banks to provide various mortgage products to Nigerians.

The mortgage-to-GDP ratio in Nigeria remains relatively low compared to more developed economies, indicating significant room for growth.

However, challenges such as high interest rates, limited long-term funding, and stringent lending criteria have historically hindered widespread mortgage adoption.

Despite these obstacles, recent government initiatives and private sector innovations are gradually making mortgages more accessible to a broader segment of the population.

Types of Mortgage Options

Nigerian homebuyers and investors can choose from several mortgage options, each with its unique features and requirements.

The most common types include:Federal Mortgage Bank of Nigeria (FMBN) Loans:

These are government-backed mortgages designed to provide affordable housing finance to Nigerian workers.

The National Housing Fund (NHF) scheme, administered by the FMBN, allows contributors to access loans at favorable interest rates for home purchase or construction.

Commercial Bank Mortgages: Many commercial banks in Nigeria offer mortgage products to their customers.

These loans typically have higher interest rates compared to government-backed options but may offer more flexibility in terms of loan amounts and repayment periods.

Primary Mortgage Bank Loans: Specialized mortgage institutions provide various home financing options, often with more competitive rates than commercial banks.

These institutions focus exclusively on mortgage lending and may offer more tailored products to meet specific needs.

Rent-to-Own Schemes: Some developers and financial institutions offer rent-to-own arrangements, allowing tenants to gradually build equity in a property while paying rent.

This option can be particularly attractive for those who may not qualify for traditional mortgages.

Cooperative Society Loans: Many Nigerians participate in cooperative societies that pool resources to provide housing loans to members.

These loans often come with lower interest rates and more flexible terms compared to traditional banking options.Eligibility and Requirements

Securing a mortgage in Nigeria typically requires meeting certain eligibility criteria and fulfilling specific requirements. While these may vary depending on the lender and the type of mortgage, common factors include:

Income and Employment:

Lenders generally require proof of stable income and employment. The debt-to-income ratio is a crucial factor in determining loan eligibility and amount.Credit History:

Although Nigeria lacks a comprehensive credit scoring system, lenders may review an applicant’s credit history and repayment record on previous loans.

Down Payment: Most mortgage options in Nigeria require a significant down payment, typically ranging from 20% to 30% of the property’s value.

Some government-backed schemes may offer lower down payment requirements.Property Valuation: The property being purchased or used as collateral must undergo a professional valuation to determine its market value and ensure it meets the lender’s criteria.

Documentation: Applicants must provide various documents, including identification, proof of income, tax clearance certificates, and property-related documents.

Age Limit: Many lenders impose age restrictions, often requiring the mortgage to be fully repaid before the borrower reaches retirement age.

Challenges and Opportunities in Nigerian Mortgage Financing.

While the Nigerian mortgage market continues to evolve, several challenges persist. High interest rates, often in double digits, make mortgages unaffordable for many Nigerians.

The lack of long-term funding sources limits the ability of lenders to offer extended repayment periods, which could make monthly payments more manageable.Land tenure issues and the complexities of property registration in some parts of the country also pose significant hurdles.

The time and cost associated with perfecting property titles can add to the overall expense of obtaining a mortgage.

However, these challenges also present opportunities for innovation in the mortgage sector. Fintech companies are entering the market with digital solutions that streamline the mortgage application and approval process.

Some lenders are exploring alternative credit scoring methods to assess creditworthiness, potentially opening up mortgage access to a broader population.

The government’s ongoing efforts to address housing deficits through initiatives like the Family Homes Fund and the National Housing Programme are creating new opportunities for affordable mortgage financing.

Additionally, the gradual development of the secondary mortgage market through the Nigeria Mortgage Refinance Company (NMRC) is expected to increase liquidity in the sector and potentially lead to more competitive mortgage rates.

Navigating the Mortgage Process.

For Nigerians considering a mortgage, thorough research and preparation are essential.

Prospective borrowers should:

● Compare offerings from multiple lenders to find the best rates and terms.

● Understand all associated costs, including processing fees, insurance, and potential penalties for early repayment.

● Seek professional advice from financial advisors or real estate experts to make informed decisions.

● Consider the long-term implications of the mortgage, including how it aligns with future financial goals and career plans.

● Stay informed about government policies and initiatives that may affect the mortgage market or provide new opportunities for home financing.

As Nigeria’s real estate market continues to grow and evolve, so too will the mortgage options available to its citizens.

By understanding the current landscape and staying informed about new developments, prospective homeowners and investors can make the most of the opportunities presented by mortgage financing in Nigeria’s dynamic real estate sector.

For personalized assistance with your property needs, contact Dennis Isong, a top Lagos realtor specializing in helping Nigerians in the diaspora own property stress-free.Contact: +2348164741041

A joint security operation against terrorists has led to the rescue of nine persons in Ekiti Local Government Area of Kwara State.

According to inside sources, Forest Guards, under the supervision of the Directorate of Security Services and working with members of the local hunters and vigilante group, embarked on bush-combing operations. They discovered a hideout of the kidnappers and engaged them.

Nine persons were rescued in two separate operations in the forest of Obbo Aiyegunle. One of the kidnappers was neutralised while others fled with gunshot injuries.

One of the rescued persons is said to be receiving medical care at an undisclosed medical facility in the local government.

News

Zamfara LG Chairman Abduction: Security operatives intensify rescue efforts

Security forces are currently conducting deliberate operations at the suspected location of the terrorists, aimed at safely rescuing the abducted Chairman.

• Family of the abducted Zamfara LG Chairman

Aliyu Danjal, Lieutenant Colonel Media Information Officer Joint Task Force (North West) Operation FANSAN YAMMA, disclosed that on hearing gunshots, troops of Operation FANSAN YAMMA responded immediately and swiftly moved to the scene where they engaged in hot pursuit of the terrorists leading to a fierce exchange of fire.

News

IGP Disu orders officers to shoot anyone carrying illegal firearms

Disu explained that the directive was backed by Force Order 237, which empowers police officers to respond immediately to armed threats without waiting for approval from superior officers.

The Inspector-General of Police, Olatunji Disu, has directed police officers across the country to shoot on sight anyone found carrying illegal firearms, as part of intensified efforts to curb insecurity.

Disu issued the directive on Friday during a stakeholders’ meeting at the Government House in Makurdi, the Benue State capital, saying the move followed President Bola Tinubu’s instruction that the lingering security crisis in the state must be brought to an end.

The police chief maintained that only authorised security personnel are legally permitted to carry firearms, warning that law enforcement agencies would no longer tolerate the unlawful possession of weapons.

” You cannot move around freely carrying arms as if there is no law and order in this country. It will not be tolerated,” he said.

Disu explained that the directive was backed by Force Order 237, which empowers police officers to respond immediately to armed threats without waiting for approval from superior officers.

Security Forces Rescue 9, Neutralise Terrorist in Kwara

Nigeria’s Enang Presents Credentials to German President Steinmeier (Images)

Zamfara LG Chairman Abduction: Security operatives intensify rescue efforts

Tech Expert, Zuckerberg trains with UFC champions, Adesanya, Alexander

Organ Trafficking: Ekweremadu bags 10 years in UK prison

SAINT OBI: Between his marriage and his death

-

News3 days ago

News3 days ago311 lawmakers say “YES!” to establish state police

-

Business2 days ago

Business2 days agoNaira Exchange Rates Across Black Market, CBN, Commercial Banks Friday, July 24

-

News3 days ago

News3 days agoSoludo’s daughter bags First Class from UK university

-

Business2 days ago

Business2 days agoMTN Nigeria asks customers to trade old SIM packs for prizes

-

News2 days ago

News2 days agoEleven poets jostle for $100,000, ‘Nigeria Prize for Literature 2026’

-

Business2 days ago

Business2 days agoUS subjects imports from Nigeria to 12.5% tariff

-

News2 days ago

News2 days agoPetrol hits N1,400/l as Brent Surges To $100

-

News3 days ago

News3 days agoSenate okays Yuguda acting in full capacity as AMCON Board chairman