Business

Access HoldCo: Roosevelt Ogbonna Quits Board in compliance with CBN regulations

Beyond his role as CEO, Mr. Ogbonna sits on the boards of Access Bank’s subsidiaries in the UK and South Africa and represents the bank on the boards of the Africa Finance Corporation and CSCS Plc.

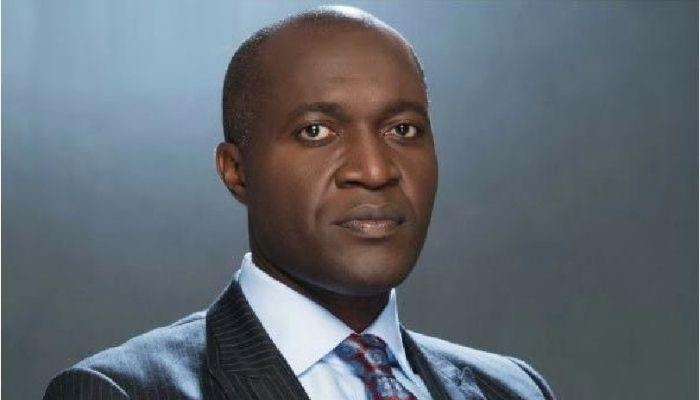

Access Holdings has confirmed the resignation of Mr. Roosevelt Ogbonna as Non-Executive Director from its Board after three and a half years of dedicated service, but remains Access Bank’s MD/CEO.

The Company Secretary, Sunday Ekwochi, said that Mr. Ogbonna will continue in his role as the Managing Director and Chief Executive Officer of Access Bank Plc, the Group’s flagship banking subsidiary.

The company explained that his resignation became necessary to ensure compliance with the Central Bank of Nigeria’s Corporate Governance Guidelines for Financial Holding Companies (2023), which limit the number of directors on a financial holding company’s board to nine.

The board appreciates Mr. Ogbonna for his outstanding and continued contributions to the Access Group,” the statement read.

Mr. Ogbonna was appointed Managing Director and Chief Executive Officer of Access Bank Plc in May 2022, after serving as Deputy Managing Director from 2017 and Executive Director from 2013.

He joined Access Bank in 2002 from Guaranty Trust Bank and has over two decades of experience in the banking sector.

A Fellow of the Institute of Chartered Accountants of Nigeria (FCA), an Honorary Member of the Chartered Institute of Bankers (HCIB), and a CFA charter holder, Mr. Ogbonna holds an MBA from IMD Business School in Switzerland, an LL.M in International Corporate & Commercial Law from King’s College London, and an Executive MBA from Cheung Kong Graduate School of Business.

He also earned a B.Sc. in Banking and Finance from the University of Nigeria, Nsukka, and completed the Senior Executive Fellow programme at Harvard Kennedy School of Government.In 2015, he was recognised by the Institute of International Finance as one of its Future Global Leaders.

Beyond his role as CEO, Mr. Ogbonna sits on the boards of Access Bank’s subsidiaries in the UK and South Africa and represents the bank on the boards of the Africa Finance Corporation and CSCS Plc.

As of August 2025, the Board of Access Holdings Plc is chaired by Aigboje Aig-Imoukhuede, with Bolaji Olaitan Agbede serving as Acting Group CEO and Lanre Bamisebi as Executive Director.

The independent non-executive directors include Abubakar Aribidesi Jimoh, Fatimah Bintah Bello-Ismail, and Ibironke Adeyemi, while other members are Ojinika Nkechinyelu Olaghere and Olusegun Babalola Ogbonne.

Business

Cardoso Urges Banks To Lend Out Idle Funds With CBN * Retains MPR at 26.5%

Cardoso made the call on Tuesday after the 306th Monetary Policy Committee (MPC) meeting held in Abuja from July 20 to July 21.

The Central Bank of Nigeria (CBN) Governor, Olayemi Cardoso , urged banks from keeping idle funds with the apex bank and encouraging increased lending into the economy.

Cardoso made the call on Tuesday after the 306th Monetary Policy Committee (MPC) meeting held in Abuja from July 20 to July 21.

The apex bank retained the Monetary Policy Rate (MPR), also known as benchmark interest rate, at 26. 5 percent.

This decision marks the second consecutive retention of the MPR at 26.5 per cent, following a 50-basis-point reduction in February from 27 per cent.

“The committee’s decision to maintain the current policy stand follows a thorough assessment of the balance of risk,” said Cardoso.

He emphasised that although headline inflation moderated marginally in June 2026, global uncertainties have heightened due mainly to the renewed hostilities in the Middle East.

The MPC also adjusted the asymmetric facilities corridor around the MPR to +50/-450 basis points—a move aimed at discouraging banks from keeping idle fund with CBN.

Furthermore, the committee maintained the Cash Reserve Ratio (CRR) for commercial banks at 45 per cent, retained the rate for merchant banks at 16 per cent, and kept the CRR on non-TSA public-sector deposits at 75 per cent for liquidity management considerations.

Cardoso said despite the global uncertainties, the Nigerian economy has “remained largely resilient to the external shocks”.

Business

CBN admits it opened domiciliary accounts for PFIPC agency

Represented by the Director of its Banking Services Department, Hamisu Ibrahim, the CBN said that the accounts are one in US dollars, the other in British pounds sterling, were opened following a mandate received from the Office of the Accountant-General of the Federation.

File photo : PFIPC agency DG, Adeniyi Adeyemi

The Central Bank of Nigeria had admitted that it opened two foreign-currency domiciliary accounts for the controversial Presidential Foreign Investment Promotion Council (PFIPC).

The apex bank made the confirmation, yesterday, during the public hearing convened at the National Assembly Complex by the House of Representatives Ad-hoc Committee investigating the existence and operations of the PFIPC, chaired by Yusuf Gagdi and inaugurated by Speaker Tajudeen Abbas.

Represented by the Director of its Banking Services Department, Hamisu Ibrahim, the CBN said that the accounts are one in US dollars, the other in British pounds sterling, were opened following a mandate received from the Office of the Accountant-General of the Federation.

He explained that on July 30, 2025, CBN received a mandate dated July 29, 2025 from the Office of the Accountant-General.

“We received the mandate to authorise two accounts, one a US dollar domiciliary account, the other a pound domiciliary account, for the Presidential Economic Advisory Council/Presidential Foreign Investment Promotion Council,” Ibrahim told the committee.

He explained the CBN’s verification process, “The process of opening an account requires a mandate from the Office of the Accountant-General of the Federation.

“Once we receive that mandate, we perform all the necessary verifications to confirm that this mandate is actually coming from that office.

The department that handles the mandate is different from the department that actually does the account opening,” he said.

Nevertheless, he noted that no one came to activate the accounts after they were opened.“We did not receive any correspondence, mandate, signature or mandate cards. We were not introduced to the authorising or approving officers.“Based on that, those accounts remain inactive, with zero balance. There have been no foreign exchange allocations.

BLACK MARKET RATES

US DOLLAR (USD) Buy ₦1, 410 Sell ₦1,415

GREAT BRITISH POUND (GBP) Buy ₦1,890 Sell: ₦1,910

EURO (EUR) Buy ₦1,580 Sell ₦1,600

CANADIAN DOLLAR (CAD) Buy ₦1,020 Sell ₦1,080

SOUTH AFRICAN RAND (ZAR) Buy ₦75 Sell ₦90

UAE DIRHAM Buy ₦350 Sell ₦370 CHINESE YUAN Buy ₦190 Sell ₦205

GHANA CEDI (GHS) Buy ₦95 Sell ₦110

WEST AFRICAN CFA Buy ₦2, 300 Sell ₦2, 400

CENTRAL AFRICAN CFA Buy ₦2,150 Sell 2,250

AUSTRALIAN DOLLAR Buy ₦800 Sell ₦900

CBN OFFICIAL EXCHANGE RATES

US DOLLAR (USD) ₦1,380.11

GREAT BRITISH POUND (GBP) ₦1,857.35

EURO (EUR) ₦1,575.95

SWISS FRANC (CHF) ₦1,705. 31

JAPANESE YEN (JPN) ₦8.50

CHINESE YUAN (CNY) ₦203.94

WEST AFRICAN CFA (XOF) ₦2.40

WEST AFRICAN UNIT ACCOUNT (WAUA) ₦1,874. 32

SAUDI RIYAL (SAR) ₦367.49

SOUTH AFRICAN RAND (ZAR) ₦83.69

Achimugu Seeks National, Global Protection Over Threats To Her Life and Businesses

Katsina Flood Sweeps Away Siblings Returning From Islamiyya School

An alleged fake university discover in Lagos

Tech Expert, Zuckerberg trains with UFC champions, Adesanya, Alexander

Organ Trafficking: Ekweremadu bags 10 years in UK prison

SAINT OBI: Between his marriage and his death

-

News2 days ago

News2 days agoBIJAMIC College Charges Class of 2026 Graduates to Embrace Resilience, Learn from Thomas Edison

-

Sports3 days ago

Sports3 days agoWho made the FIFA World Cup trophy?

-

Crime2 days ago

Crime2 days agoStudents Killed as Troops Foil ISWAP Abduction Bid in Borno

-

Sports2 days ago

Sports2 days agoFIFA To Review Hydration Breaks After World Cup Final – Wenger

-

News2 days ago

News2 days agoBadejo-Okusanya Emerges NBA National President (2026-2028)

-

News2 days ago

News2 days agoSenegal President, Faye elected new ECOWAS chairman

-

Sports2 days ago

Sports2 days agoEngland beat France 6-4 to claim World Cup third place

-

News2 days ago

News2 days agoAbbas inaugurating today committee to investigate illegal PFIPC agency