Business

Real Estate Due Diligence: What Every Buyer Must Check Before Paying in Lagos State by Dennis Isong

Avoid lands tagged as “committed”—this means the government has already planned something for that area.

Mr. Samuel had finally saved enough to buy his dream plot in Lagos. He was tired of renting and wanted a piece of land to call his own.

One day, he came across a well-dressed agent who promised him a juicy deal—a prime piece of land in Ibeju-Lekki at an unbelievably low price.

The agent assured him that everything was “clean.” No Omo Onile drama, no government wahala. Mr. Samuel was excited.

He visited the land once, saw a few other buyers inspecting, and felt reassured. Without conducting any serious checks, he quickly made payment.

The agent even arranged for a “lawyer” to draft a deed of assignment. Everything seemed perfect.

Two months later, Mr. Samuel decided to start building. That was when the nightmare began. A group of fierce-looking men stormed the site, shouting that the land belonged to their family.

They claimed they never sold it to anyone. Confused and scared, Mr. Samuel tried calling the agent—his number was switched off.

The “lawyer” who drafted his deed had disappeared too. He went to the Lagos State Land Registry, only to discover that the land was government-acquired. Mr. Samuel had lost everything.

His hard-earned savings, his dreams, and his peace of mind. This could have been avoided if only he had done proper due diligence before paying.

What is Due Diligence in Real Estate?

Due diligence means verifying everything about a property before committing to buy it. It’s like running a background check to make sure you are not about to throw your money into a trap.

Lagos is notorious for real estate fraud—Omo Onile disputes, fake land documents, and government-acquired properties being resold illegally. One wrong move and you could lose millions.

So, before you pay a kobo, here are the critical things you must check:

1. Confirm Ownership: Who Really Owns the Land?

Never assume the person selling the land is the real owner. People sell land they don’t own every day in Lagos. Some are tenants or relatives of the real owner, while others are pure scammers.

What to Do:

● Ask for the title documents (C of O, Deed of Assignment, Governor’s Consent, or Survey Plan).

● Go to the Lagos State Land Registry (Alausa) to verify the document. If the land is not registered, don’t buy it.

● If it’s family land, ensure all family members involved sign the documents to avoid future disputes.

2. Verify Land Title and Documents

Even if the seller shows you a C of O, don’t trust it blindly. Fake C of Os and land documents flood the market. Some lands also have government restrictions, meaning they can be demolished anytime.

What to Do:

● Conduct a search at the Lagos State Lands Bureau to verify if the title is genuine.

● Cross-check survey plans at the Office of the Surveyor-General to confirm the land’s coordinates and whether it falls under government acquisition.

● Engage a trusted real estate lawyer to help you review the documents.

3. Check for Government Acquisition Issues Lagos State is aggressive when it comes to land acquisition. Some lands are meant for future government projects but are still being illegally sold to unsuspecting buyers.

What to Do: ● Visit the Lagos State Ministry of Physical Planning and Urban Development to check if the land is under acquisition.

● Avoid lands tagged as “committed”—this means the government has already planned something for that area.

4. Conduct a Physical Inspection—Don’t Rely on Photos Many buyers have fallen victim to real estate scams because they paid for land they never saw. Some agents take buyers to a different land, collect money, and disappear.

What to Do:

● Visit the land multiple times—morning, afternoon, and evening. ● Talk to neighbors and ask questions about the land’s history.

● Check for any signs of disputes (e.g., different people laying claims to the land).

5. Avoid Verbal Agreements—Everything Must Be in Writing Many people have lost money because they trusted verbal agreements. Some sellers will promise you land and later deny ever meeting you.

What to Do:

● Ensure you have a proper sales agreement signed by both parties.

● The agreement should be prepared by a trusted lawyer, not the seller’s lawyer (to avoid conflict of interest).

● Every payment must be documented, and receipts issued.

6. Investigate the Seller or Real Estate Company Some real estate companies in Lagos operate like Ponzi schemes.

They sell lands that don’t belong to them, promising fake allocations.

Before you pay, verify! Before you sign, investigate! Before you trust, confirm! And if you need expert guidance, reach out to a trusted real estate professional (like me) who can help you avoid the pitfalls.

What to Do:

● Research the company’s history and reviews from past buyers.

● Confirm their RC number and check if they are registered with CAC.

● Visit their physical office and ask tough questions. 7. Beware of Omo Onile Wahala Omo Onile (land grabbers) can frustrate landowners with illegal fees and disturbances.

They can show up after purchase, demanding extra money or threatening to seize the land.

What to Do:

● Buy land in secured estates to avoid Omo Onile drama.

● If buying directly from a family, ensure ALL family members agree to the sale.

● Have a lawyer draft an indemnity clause in your agreement to protect you from future Omo Onile claims.

8. Know the Land Use Purpose

Not all lands are meant for residential buildings. Some are strictly for commercial, agricultural, or industrial use.

What to Do:

● Check the zoning regulations at the Lagos State Ministry of Physical Planning.

● If you’re buying for business, ensure you won’t run into legal troubles later.

Don’t Let Greed and Urgency Lead You Into a Trap Many people fall victim to real estate scams because they are in a rush or want “cheap land.”

Lagos is a tough market—if a deal looks too good to be true, it probably is.

Remember Mr. Ade’s story? Don’t let it happen to you. No matter how urgent the deal seems, take your time to verify everything.

Due diligence is not a waste of time; it’s the only thing standing between you and financial disaster.

Before you pay, verify! Before you sign, investigate! Before you trust, confirm! And if you need expert guidance, reach out to a trusted real estate professional (like me) who can help you avoid the pitfalls.

Business

33 Nigerian Banks Beat CBN’s Recapialisation with ₦4.65trn Combined Capital Base

The recapitalisation programme has strengthened the capital base of Nigerian banks, reinforcing the resilience of the financial system and ensuring it is wellpositioned to support economic growth and withstand domestic and external shocks.”

•Governor of CBN, Olayemi Cardoso

The Central Bank of Nigeria (CBN) has wrapped up the banking sector recapitalisation programme it introduced two years ago (March 2024-March 31, 2026) with 33 banks successfully met the requirements deadline.

The banks raised a total of ₦4.65 trillion in new capital, according to a statement signed by Olubukola A. Akinwunmi, the Director, Banking Supervision and Hakama Sidi Ali (Mrs.), the Ag. Director, Corporate Communications.

It said that the recapialisation exercises recorded strong participation from both domestic and international investors, with 72.55% of capital sourced locally and 27.45% from international markets, reflecting sustained confidence in the Nigerian banking sector.

The statement noted that the Governor of CBN, Olayemi Cardoso said “the recapitalisation programme has strengthened the capital base of Nigerian banks, reinforcing the resilience of the financial system and ensuring it is wellpositioned to support economic growth and withstand domestic and external shocks.”

“The CBN confirms that 33 banks have met the revised minimum capital requirements established under the programme.

A limited number of institutions remain subject to ongoing regulatory and judicial processes, which are being addressed through established supervisory and legal frameworks.

“All banks remain fully operational, ensuring continued access to banking services for customers.

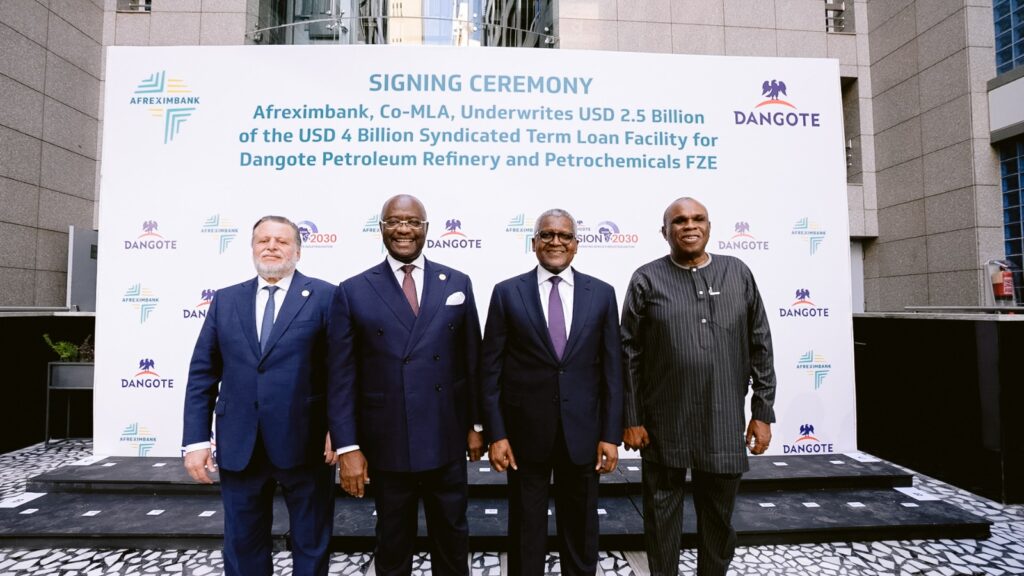

African Export-Import Bank has underwritten $2.5 billion in a $4 billion senior syndicated term loan for Dangote Petroleum Refinery and Petrochemicals, in a move aimed at strengthening the refinery’s financial position and supporting its long-term growth and expansion strategy.

The five-year facility, arranged alongside Access Bank as co-Mandated Lead Arrangers, is designed to consolidate existing debt, optimise the refinery’s capital structure and align its financing with current operational realities.

The transaction marks a significant milestone for the Dangote Refinery, Africa’s largest refining and petrochemical complex with a capacity of 650,000 barrels per day.

Afreximbank’s $2.5 billion participation represents the largest share of the syndicate, underscoring its strategic role in mobilising capital for industrial projects across the continent.

The bank said the financing aligns with its mandate to promote industrialisation, reduce reliance on imported petroleum products and deepen intra-African trade.

Since refining operations commenced in February 2024, Afreximbank has played a key role in supporting the project, including providing a $1 billion working capital facility and acting as financial adviser on the Naira-for-Crude initiative, which facilitates crude procurement and product sales in local currency.

Speaking during a strategy session in Cairo, Egypt, President and Chairman of the Board of Directors of Afreximbank, George Elombi, said the bank’s continued backing reflects confidence in indigenous African enterprises.

“We take immense pride in being the single largest provider of financing to the Dangote Group. We do so primarily because Dangote is African,” he said.

“When we invest in ourselves, we do more than create jobs and wealth or expand government revenues; we build a secure and resilient future for our continent”

Elombi disclosed that Afreximbank has committed about $15 billion to Dangote Group since 2015, highlighting the scale of its long-term partnership with the conglomerate.

President and Chief Executive of Dangote Industries Limited, Aliko Dangote, described the financing as a critical step in positioning the refinery for its next phase of expansion.

“This financing marks an important step in strengthening the financial foundation of Dangote Petroleum Refinery & Petrochemicals and positions the business for the next phase of its growth,” he said.

“We appreciate Afreximbank’s continued support and confidence in our vision to build world-class industrial capacity that serves Nigeria, Africa and global markets.”

The syndicated loan attracted strong participation from a mix of African and international financial institutions, reflecting sustained investor confidence in the refinery as a transformative industrial asset in advancing Africa’s energy security, reducing import dependence and supporting the continent’s broader industrialisation agenda.

Business

BUA Foods Plc Reports Strong 2025 Performance with ₦1.77 Trillion Revenue, Proposes Record ₦28 Dividend per Share

Leading Nigerian food manufacturer BUA Foods Plc has announced robust full-year 2025 audited results, with revenue climbing 16% to ₦1.77 trillion from ₦1.53 trillion in 2024.

The growth was driven by sustained consumer demand for the company’s core staples sugar, flour, pasta, and rice alongside higher sales volumes and strategic pricing amid a challenging economic environment marked by inflationary pressures on households.

Profit after tax nearly doubled, rising 95% to ₦518.4 billion, while gross profit surged to ₦737.3 billion from ₦540.8 billion the previous year.

Operating profit also increased significantly to ₦656.6 billion.In a strong signal of confidence in its outlook and commitment to shareholder value, the Board of Directors has proposed a final dividend of ₦28 per ordinary share of 50 kobo.

This represents a 115% increase from the ₦13 per share paid in 2024, translating to a total payout of approximately ₦504 billion, subject to approval by shareholders at the company’s 2026 Annual General Meeting.

Chairman Abdul Samad Rabiu highlighted the results, stating that the substantial dividend hike underscores the company’s dedication to rewarding investors while continuing to invest in business expansion and operational efficiency.

BUA Foods, a major player in Nigeria’s food processing sector controlled by billionaire Abdul Samad Rabiu, has continued to benefit from scale advantages, market expansion, and resilient demand for essential food products despite broader economic headwinds.

The company’s shares have reacted positively in recent trading, reflecting investor optimism over the strong earnings and generous dividend proposal.

Full details of the financial statements were filed with the Nigerian Exchange (NGX) on Monday.

Analysts view the performance as a testament to BUA Foods’ robust business model and ability to navigate Nigeria’s macroeconomic challenges through volume growth and cost discipline.

FIFA ranks Super Eagles third in Africa, 26th globally

Police must pay transport fares, says AIG

Tinubu scurries to Jos after Mutfwang’s security brief

Tech Expert, Zuckerberg trains with UFC champions, Adesanya, Alexander

Organ Trafficking: Ekweremadu bags 10 years in UK prison

SAINT OBI: Between his marriage and his death

-

Business2 days ago

Business2 days agoBUA Foods Plc Reports Strong 2025 Performance with ₦1.77 Trillion Revenue, Proposes Record ₦28 Dividend per Share

-

News2 days ago

News2 days agoNELFUND Debunks Claims of ₦25,000 Student Upkeep Allowance

-

Politics3 days ago

Politics3 days agoPDP will contest 2027 polls, says Wike

-

Politics3 days ago

Politics3 days agoPDP Leadership Crisis: Faction Heads to Supreme Court as Tussle Deepens

-

Business3 days ago

Business3 days agoOPay launches new office in Jos

-

News3 days ago

News3 days agoLagos High Court Embraces Full Digital Transformation with Mandatory E-Filing

-

Crime3 days ago

Crime3 days agoJUST IN: Terrorists Invade Kaduna Wedding Ceremony, Kill 13 Guests In Late-Night Attack

-

Business11 hours ago

Business11 hours ago33 Nigerian Banks Beat CBN’s Recapialisation with ₦4.65trn Combined Capital Base