Business

2025: What Investors Need to Know About the Market of Property Investment in Nigeria by Dennis Isong

Think about Lekki in Lagos—just a few years ago, it was mostly bush, but today, it’s prime property.

Investing in Nigerian real estate is like planting a fruit tree—there’s effort, patience, and planning involved, but when it grows, it yields rewards for years.

Nigeria’s property market is full of opportunities, but it can be tricky for investors without the right knowledge.

Let’s break it down simply, so you know what to expect.

1. Nigeria’s Population is an Advantage Nigeria is Africa’s most populous country, with over 200 million people.

That’s a lot of people needing homes, offices, schools, and businesses!

This population growth creates a constant demand for properties. So, whether you’re investing in residential housing, commercial properties, or even land banking, you’re tapping into a growing market.

Quick Tip: Focus on areas with rising populations, like Lagos, Abuja, Port Harcourt, and emerging cities like Ibadan or Enugu.

2. Land is King In Nigeria, land is one of the safest investments. Unlike buildings that can deteriorate, land appreciates over time, especially in growing areas.

Think about Lekki in Lagos—just a few years ago, it was mostly bush, but today, it’s prime property.

What to Watch Out For:

● Ensure the land has proper documents like a Certificate of Occupancy (C of O) or a Governor’s Consent.

● Avoid omo-onile troubles by buying from reputable sellers or companies.

3. The Power of Location Location is everything in real estate.

A property in a developed area with good roads, schools, and electricity will fetch more value than one in a remote, inaccessible location. For instance:

● Lagos Island (Ikoyi, Victoria Island, Lekki): Good for high-end properties.

● Mainland (Ikeja, Yaba, Surulere): Perfect for mid-range investments.

● Emerging suburbs (Epe, Ibeju-Lekki): Great for long-term investments. Golden Rule: Research the area thoroughly.

Visit the property site, ask questions, and observe the neighborhood.

4. Real Estate Investment is Not a Sprint Let’s be honest—property investment isn’t for the impatient.

While quick flips (buying and selling quickly) can happen, most returns in real estate come over time. Whether it’s rental income, land appreciation, or property resale, you need patience.

Example: If you buy land in Epe for ₦1 million today, it might not appreciate significantly in the next year. But in 5–10 years, it could be worth ₦10 million or more!

5. Diversify Your Portfolio Don’t put all your eggs in one basket.

Mix things up! You can invest in:

● Residential properties: Apartments, duplexes, or bungalows.

● Commercial properties: Shops, offices, or warehouses.

● Land banking: Buying and holding land for future resale. By diversifying, you reduce risks and open up multiple income streams. 6. Know the Risks and How to Avoid Them Like every business, real estate has its risks:

● Legal Issues: Fake land documents, disputes, or government acquisition.

● Market Trends: Property values can fluctuate, depending on the economy.

● Maintenance Costs: Properties need upkeep, especially rental ones.

How to Reduce Risks:

● Work with trusted real estate agents or companies.

● Verify property documents with lawyers.

● Research market trends before investing. 7. Explore Financing Options You don’t need to be a billionaire to invest in Nigerian real estate. There are financing options like:

● Mortgage loans: Offered by banks and mortgage institutions.

● Co-investing: Partnering with others to buy a property.

● Installment plans: Some developers allow you to pay in bits over time. Pro Tip: Understand the terms of any loan or payment plan. Ensure it aligns with your financial capacity.

8. Rental Income is a Goldmine One of the easiest ways to make money from real estate is through rentals.

Whether it’s residential apartments, office spaces, or short-term rentals (like Airbnb), rental income provides steady cash flow.

What You Should Know:

● Properties close to universities, business hubs, or major roads attract higher rents.

● Tenants expect basic amenities like water, electricity, and security.

9. Emerging Trends in Nigerian Real Estate.

The Nigerian property market is evolving. Some trends to keep an eye on include:

● Smart Homes: Technology-driven homes with automated features.

● Co-Working Spaces: As remote work rises, shared office spaces are gaining popularity.

● Affordable Housing: Developers are targeting middle and low-income earners with budget-friendly homes.

Being aware of these trends can help you position your investments for the future. 10. Start Small and Grow Many people think they need millions to start investing in real estate. That’s not always true.

You can start small and grow.

For instance:

● Buy a small piece of land in an upcoming area.

● Invest in a one-bedroom apartment for rent. ● Partner with others to co-own a property.

11. The Role of Real Estate Agents and Experts

Don’t try to do everything alone. Real estate agents, surveyors, and lawyers are your friends in this journey.

They’ll help you navigate the complex process of buying, selling, or renting properties. Dennis Isong’s Advice: Always work with professionals who have a track record of honesty and success in the market.

12. Tax and Regulatory Issues Don’t forget that property investment comes with taxes and regulations.

For instance:

● Land Use Charge: Payable annually on properties in Lagos.

● Capital Gains Tax: When you sell a property at a profit. Stay updated on these requirements to avoid penalties.

13. Opportunities in Rural Areas Urban areas like Lagos and Abuja may dominate headlines, but rural areas also hold potential.

As Nigeria develops, rural areas are turning into new hotspots for businesses and housing.

For example:

● Invest in farmland for agriculture.

● Buy land near upcoming government projects, like roads or airports.

14. Never Stop Learning

The real estate market is dynamic. New laws, trends, and opportunities arise frequently.

As infrastructure in Epe improves through government-funded projects supported by tax reforms, your land value appreciates significantly. Over 5–10 years, your property could fetch a value of ₦15 million, yielding substantial returns.

To stay ahead, keep learning:

● Attend real estate seminars.

● Follow market news.

● Network with other investors. The recent tax reform and changes in bank charges in Nigeria have significant implications for real estate investors, both positive and challenging.

Incorporating these developments into your investment strategy can help you maximize returns and minimize risks.

15. Impact of Tax Reforms on Real Estate The Nigerian government has introduced reforms aimed at streamlining tax collection and fostering economic growth.

These changes have direct and indirect benefits for real estate investors: a. Lower Compliance Costs Streamlined tax processes reduce bureaucratic delays, making it easier for property owners to comply with tax obligations like Land Use Charges and Capital Gains Tax. This clarity ensures fewer penalties and better financial planning. b. Improved Infrastructure Development Tax revenues are increasingly being channeled into infrastructure development, such as roads, railways, and power projects.

This directly boosts property values, especially in areas where such projects are underway, like Epe, Ibeju-Lekki, and the outskirts of Abuja. c. Incentives for Affordable Housing

To address Nigeria’s housing deficit, tax incentives are now available for developers investing in low-income housing.

This creates opportunities for investors to partner with developers or invest in projects targeting middle and low-income earners.

How to Benefit:

● Stay informed about tax reforms through newsletters and government updates.

● Take advantage of tax holidays and exemptions available for certain real estate developments.

16. Bank Charges and Real Estate Financing

The Central Bank of Nigeria (CBN) has recently revised bank charges, which affects how investors access financing.

Here’s how this impacts your real estate investments:

a. Lower Transaction Costs Reduced charges for bank transfers and e-banking services make it cheaper to process payments, whether you’re paying for land, construction materials, or rental income management.

b. Accessible Mortgage Loans Banks are under pressure to make mortgage loans more accessible and affordable.

Lower interest rates and reduced processing fees are encouraging more Nigerians to consider homeownership or property investment.

c. Easier Installment Payments For installment plans offered by developers, lower bank charges mean fewer deductions on recurring payments. This makes it easier for investors to stick to payment schedules.

How to Benefit:

● Negotiate favorable terms with banks, especially for long-term property loans.

● Use e-banking platforms to save on transaction fees when making payments.

Practical Example Imagine you purchase land in Epe for ₦2 million using a bank loan.

With reduced interest rates and minimal transfer charges, you save money both on the initial payment and subsequent installments.

As infrastructure in Epe improves through government-funded projects supported by tax reforms, your land value appreciates significantly. Over 5–10 years, your property could fetch a value of ₦15 million, yielding substantial returns.

Key Takeaways

● Understand Tax Benefits: Take full advantage of tax reforms and incentives for real estate development.

● Leverage Affordable Financing: Use reduced bank charges and improved mortgage options to your advantage.

● Plan for Growth: Invest in areas benefiting from infrastructure projects funded by tax revenues. By incorporating these reforms into your real estate strategy, you position yourself to thrive in Nigeria’s evolving property market.

Keep learning, stay patient, and make informed decisions to secure your financial future.

In Conclusion

The Nigerian property market is a land of opportunities, but it’s not without challenges.

With the right knowledge, planning, and patience, you can turn your investment into a goldmine.

Remember: Start small, think long-term, and always consult experts when in doubt.

Real estate is a journey, and every smart step you take brings you closer to financial freedom.

STOP LOSING MONEY IN LAGOS REAL ESTATE!. Learn How to Verify Land Titles, Avoid Scams, and Make Smart Investments.

Click to Learn About Real Estate Due Diligence Now!=>> https://landproperty.ng/free

Your Investment Deserves Protection.

Business

33 Nigerian Banks Beat CBN’s Recapialisation with ₦4.65trn Combined Capital Base

The recapitalisation programme has strengthened the capital base of Nigerian banks, reinforcing the resilience of the financial system and ensuring it is wellpositioned to support economic growth and withstand domestic and external shocks.”

•Governor of CBN, Olayemi Cardoso

The Central Bank of Nigeria (CBN) has wrapped up the banking sector recapitalisation programme it introduced two years ago (March 2024-March 31, 2026) with 33 banks successfully met the requirements deadline.

The banks raised a total of ₦4.65 trillion in new capital, according to a statement signed by Olubukola A. Akinwunmi, the Director, Banking Supervision and Hakama Sidi Ali (Mrs.), the Ag. Director, Corporate Communications.

It said that the recapialisation exercises recorded strong participation from both domestic and international investors, with 72.55% of capital sourced locally and 27.45% from international markets, reflecting sustained confidence in the Nigerian banking sector.

The statement noted that the Governor of CBN, Olayemi Cardoso said “the recapitalisation programme has strengthened the capital base of Nigerian banks, reinforcing the resilience of the financial system and ensuring it is wellpositioned to support economic growth and withstand domestic and external shocks.”

“The CBN confirms that 33 banks have met the revised minimum capital requirements established under the programme.

A limited number of institutions remain subject to ongoing regulatory and judicial processes, which are being addressed through established supervisory and legal frameworks.

“All banks remain fully operational, ensuring continued access to banking services for customers.

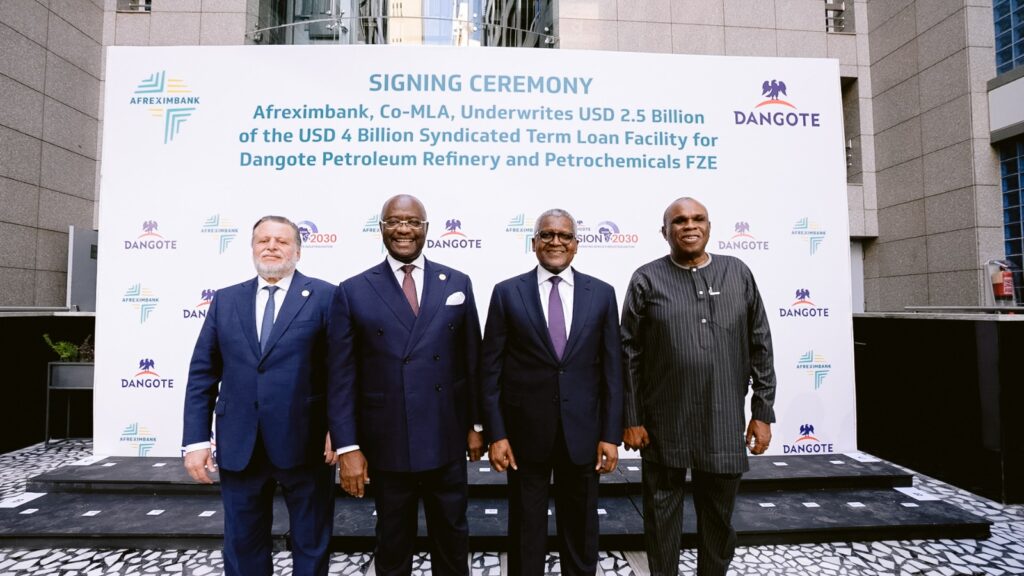

African Export-Import Bank has underwritten $2.5 billion in a $4 billion senior syndicated term loan for Dangote Petroleum Refinery and Petrochemicals, in a move aimed at strengthening the refinery’s financial position and supporting its long-term growth and expansion strategy.

The five-year facility, arranged alongside Access Bank as co-Mandated Lead Arrangers, is designed to consolidate existing debt, optimise the refinery’s capital structure and align its financing with current operational realities.

The transaction marks a significant milestone for the Dangote Refinery, Africa’s largest refining and petrochemical complex with a capacity of 650,000 barrels per day.

Afreximbank’s $2.5 billion participation represents the largest share of the syndicate, underscoring its strategic role in mobilising capital for industrial projects across the continent.

The bank said the financing aligns with its mandate to promote industrialisation, reduce reliance on imported petroleum products and deepen intra-African trade.

Since refining operations commenced in February 2024, Afreximbank has played a key role in supporting the project, including providing a $1 billion working capital facility and acting as financial adviser on the Naira-for-Crude initiative, which facilitates crude procurement and product sales in local currency.

Speaking during a strategy session in Cairo, Egypt, President and Chairman of the Board of Directors of Afreximbank, George Elombi, said the bank’s continued backing reflects confidence in indigenous African enterprises.

“We take immense pride in being the single largest provider of financing to the Dangote Group. We do so primarily because Dangote is African,” he said.

“When we invest in ourselves, we do more than create jobs and wealth or expand government revenues; we build a secure and resilient future for our continent”

Elombi disclosed that Afreximbank has committed about $15 billion to Dangote Group since 2015, highlighting the scale of its long-term partnership with the conglomerate.

President and Chief Executive of Dangote Industries Limited, Aliko Dangote, described the financing as a critical step in positioning the refinery for its next phase of expansion.

“This financing marks an important step in strengthening the financial foundation of Dangote Petroleum Refinery & Petrochemicals and positions the business for the next phase of its growth,” he said.

“We appreciate Afreximbank’s continued support and confidence in our vision to build world-class industrial capacity that serves Nigeria, Africa and global markets.”

The syndicated loan attracted strong participation from a mix of African and international financial institutions, reflecting sustained investor confidence in the refinery as a transformative industrial asset in advancing Africa’s energy security, reducing import dependence and supporting the continent’s broader industrialisation agenda.

Business

BUA Foods Plc Reports Strong 2025 Performance with ₦1.77 Trillion Revenue, Proposes Record ₦28 Dividend per Share

Leading Nigerian food manufacturer BUA Foods Plc has announced robust full-year 2025 audited results, with revenue climbing 16% to ₦1.77 trillion from ₦1.53 trillion in 2024.

The growth was driven by sustained consumer demand for the company’s core staples sugar, flour, pasta, and rice alongside higher sales volumes and strategic pricing amid a challenging economic environment marked by inflationary pressures on households.

Profit after tax nearly doubled, rising 95% to ₦518.4 billion, while gross profit surged to ₦737.3 billion from ₦540.8 billion the previous year.

Operating profit also increased significantly to ₦656.6 billion.In a strong signal of confidence in its outlook and commitment to shareholder value, the Board of Directors has proposed a final dividend of ₦28 per ordinary share of 50 kobo.

This represents a 115% increase from the ₦13 per share paid in 2024, translating to a total payout of approximately ₦504 billion, subject to approval by shareholders at the company’s 2026 Annual General Meeting.

Chairman Abdul Samad Rabiu highlighted the results, stating that the substantial dividend hike underscores the company’s dedication to rewarding investors while continuing to invest in business expansion and operational efficiency.

BUA Foods, a major player in Nigeria’s food processing sector controlled by billionaire Abdul Samad Rabiu, has continued to benefit from scale advantages, market expansion, and resilient demand for essential food products despite broader economic headwinds.

The company’s shares have reacted positively in recent trading, reflecting investor optimism over the strong earnings and generous dividend proposal.

Full details of the financial statements were filed with the Nigerian Exchange (NGX) on Monday.

Analysts view the performance as a testament to BUA Foods’ robust business model and ability to navigate Nigeria’s macroeconomic challenges through volume growth and cost discipline.

Lagos Fanti carnival holds tomorrow at TBS and environs

Atiku hires US lobbying firm for $1.2m to boost image – Report

Kaduna Mando Garage Explosion Not Bomb- Police

Tech Expert, Zuckerberg trains with UFC champions, Adesanya, Alexander

Organ Trafficking: Ekweremadu bags 10 years in UK prison

SAINT OBI: Between his marriage and his death

-

Politics2 days ago

Politics2 days agoINEC Dismisses Calls for Chairman’s Removal

-

Crime1 day ago

Crime1 day agoThree Killed, One Injured in Fresh Jos Attack (Video)

-

News3 hours ago

News3 hours agoKaduna Mando Garage Explosion Not Bomb- Police

-

Politics2 days ago

Politics2 days agoOnyejeocha resigns as Minister of State for Labour

-

News3 hours ago

News3 hours agoAtiku hires US lobbying firm for $1.2m to boost image – Report

-

Politics2 days ago

Politics2 days agoLabour Party to hold presidential primary April 28

-

Politics2 days ago

Politics2 days agoNo force can defeat Tinubu in 2027 –Umahi

-

News1 day ago

News1 day agoNigerian Army Debunks Claims of Attack on Bishop Matthew Kukah’s Residence and Sokoto Catholic Cathedral