Business

WhatsApp may exit Nigeria over $220m fine

One week after Nigeria’s Federal Competition and Consumer Protection Commission imposed a $220 million fine on WhatsApp for a data privacy breach, the company may suspend its operations in the country due to further regulatory demands.

Sources close to the situation indicate that Meta, WhatsApp’s parent company, is contemplating the withdrawal of certain services from Nigeria.

Alongside the substantial fine, the FCCPC has directed WhatsApp to cease sharing user data with other Facebook companies and third parties without explicit user consent.

The commission also requires WhatsApp to disclose details about its data collection practices and to enhance user control over data usage.

In response, a WhatsApp spokesperson emailed TechCabal, “We want to be clear that, technically, based on the order, it would be impossible to provide WhatsApp in Nigeria or globally.

” The spokesperson criticized the FCCPC’s order as flawed, asserting that it inaccurately portrays WhatsApp’s data handling and would necessitate significant changes to the platform’s infrastructure.

Meta has not addressed the FCCPC’s allegations regarding user opt-out options from the 2021 privacy policy but maintains that the update does not involve sharing user data.

The company’s privacy policy states, “While traditionally mobile carriers and operators store this information, we believe that keeping these records for two billion users would be both a privacy and security risk and we don’t do it.”

The potential suspension of WhatsApp could have significant repercussions for individuals and small businesses in Nigeria, many of whom rely on WhatsApp, Instagram, and Facebook for customer engagement.

Some privacy lawyers have questioned the FCCPC’s use of the National Data Protection Regulation as the foundation for the fine.

Enacted in 2019 by the National Information Technology Development Agency, the NDPR is Nigeria’s principal data protection framework.

Two unnamed lawyers have expressed doubts about the NDPR’s authority in such a high-stakes matter and questioned whether a government regulation can be deemed definitive in privacy issues.

Additionally, two unnamed government officials have raised concerns about the fairness of the $220 million fine. “We are too revenue-focused.

What is the opportunity cost of $220 million in government coffers?” questioned an industry expert.

Should WhatsApp choose to halt its operations in Nigeria due to these demands, both the FCCPC and the Nigerian government will face significant scrutiny and consequences.

Business

President Tinubu Approves N3.3Trn Payments Plan To Restore Reliable Electricity

Implementation has begun, with 15 power plants signing settlement agreements totalling ₦2.3 trillion.

President Bola Tinubu has approved the payment plan to finally settle the outstanding debts under the Presidential Power Sector Financial Reforms Programme.

The debt repayment plan followed the final review of the legacy debts that have beset the power sector for more than a decade.

State House press release signed by Bayo Onanuga Special Adviser to the President(Information and Strategy), said that the long-standing debts accumulated between February 2015 and March 2025.

Following verification, ₦3.3 trillion has been agreed as a full and final settlement, ensuring a fair and transparent resolution.

Implementation has begun, with 15 power plants signing settlement agreements totalling ₦2.3 trillion.

The Federal Government has already raised ₦501 billion to fund these payments.

Out of the amount, N223 billion has been disbursed, with further payments underway.

What this means for Nigerians: With payments reaching the power value chain, generation will be more stable. With power plants supported, electricity reliability will improve.

And as the sector stabilises, more investment, more jobs, and better service will follow. “This programme is not just about settling legacy debts.

It is about restoring confidence across the power sector — ensuring gas suppliers are paid, power plants can keep running, and the system begins to work more reliably”, explained Olu Arowolo-Verheijen, Special Adviser on Energy to President Tinubu.

“It is part of a broader set of reforms already underway — including better metering and service-based tariffs that link what you pay to the quality of electricity you receive.

“The government is also prioritising power supply to businesses, industries, and small enterprises — because reliable electricity is critical to creating jobs, supporting livelihoods, and growing the economy.

“The goal is simple: more reliable power for homes, stronger support for businesses, and a system that works better for all Nigerians”, she added.

President Tinubu has commended all stakeholders who supported efforts to resolve the legacy issues in the power sector.

He has also confirmed that the next phase (Series II) will begin this quarter.

Business

33 Nigerian Banks Beat CBN’s Recapialisation with ₦4.65trn Combined Capital Base

The recapitalisation programme has strengthened the capital base of Nigerian banks, reinforcing the resilience of the financial system and ensuring it is wellpositioned to support economic growth and withstand domestic and external shocks.”

•Governor of CBN, Olayemi Cardoso

The Central Bank of Nigeria (CBN) has wrapped up the banking sector recapitalisation programme it introduced two years ago (March 2024-March 31, 2026) with 33 banks successfully met the requirements deadline.

The banks raised a total of ₦4.65 trillion in new capital, according to a statement signed by Olubukola A. Akinwunmi, the Director, Banking Supervision and Hakama Sidi Ali (Mrs.), the Ag. Director, Corporate Communications.

It said that the recapialisation exercises recorded strong participation from both domestic and international investors, with 72.55% of capital sourced locally and 27.45% from international markets, reflecting sustained confidence in the Nigerian banking sector.

The statement noted that the Governor of CBN, Olayemi Cardoso said “the recapitalisation programme has strengthened the capital base of Nigerian banks, reinforcing the resilience of the financial system and ensuring it is wellpositioned to support economic growth and withstand domestic and external shocks.”

“The CBN confirms that 33 banks have met the revised minimum capital requirements established under the programme.

A limited number of institutions remain subject to ongoing regulatory and judicial processes, which are being addressed through established supervisory and legal frameworks.

“All banks remain fully operational, ensuring continued access to banking services for customers.

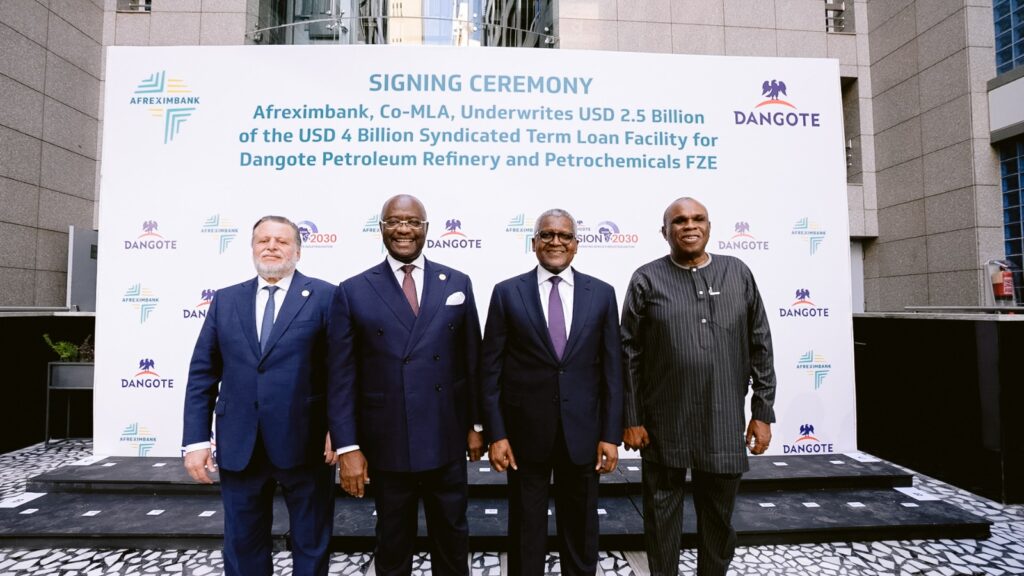

African Export-Import Bank has underwritten $2.5 billion in a $4 billion senior syndicated term loan for Dangote Petroleum Refinery and Petrochemicals, in a move aimed at strengthening the refinery’s financial position and supporting its long-term growth and expansion strategy.

The five-year facility, arranged alongside Access Bank as co-Mandated Lead Arrangers, is designed to consolidate existing debt, optimise the refinery’s capital structure and align its financing with current operational realities.

The transaction marks a significant milestone for the Dangote Refinery, Africa’s largest refining and petrochemical complex with a capacity of 650,000 barrels per day.

Afreximbank’s $2.5 billion participation represents the largest share of the syndicate, underscoring its strategic role in mobilising capital for industrial projects across the continent.

The bank said the financing aligns with its mandate to promote industrialisation, reduce reliance on imported petroleum products and deepen intra-African trade.

Since refining operations commenced in February 2024, Afreximbank has played a key role in supporting the project, including providing a $1 billion working capital facility and acting as financial adviser on the Naira-for-Crude initiative, which facilitates crude procurement and product sales in local currency.

Speaking during a strategy session in Cairo, Egypt, President and Chairman of the Board of Directors of Afreximbank, George Elombi, said the bank’s continued backing reflects confidence in indigenous African enterprises.

“We take immense pride in being the single largest provider of financing to the Dangote Group. We do so primarily because Dangote is African,” he said.

“When we invest in ourselves, we do more than create jobs and wealth or expand government revenues; we build a secure and resilient future for our continent”

Elombi disclosed that Afreximbank has committed about $15 billion to Dangote Group since 2015, highlighting the scale of its long-term partnership with the conglomerate.

President and Chief Executive of Dangote Industries Limited, Aliko Dangote, described the financing as a critical step in positioning the refinery for its next phase of expansion.

“This financing marks an important step in strengthening the financial foundation of Dangote Petroleum Refinery & Petrochemicals and positions the business for the next phase of its growth,” he said.

“We appreciate Afreximbank’s continued support and confidence in our vision to build world-class industrial capacity that serves Nigeria, Africa and global markets.”

The syndicated loan attracted strong participation from a mix of African and international financial institutions, reflecting sustained investor confidence in the refinery as a transformative industrial asset in advancing Africa’s energy security, reducing import dependence and supporting the continent’s broader industrialisation agenda.

Trump orders Iran to open Strait of Hormuz by Tuesday or face ‘hell’

Women giving birth on their backs or squatting – Which is Better?

2027: Atiku Vows To Support Whoever Emerges ADC Presidential Candidate

Tech Expert, Zuckerberg trains with UFC champions, Adesanya, Alexander

Organ Trafficking: Ekweremadu bags 10 years in UK prison

SAINT OBI: Between his marriage and his death

-

Crime2 days ago

Crime2 days agoThree Killed, One Injured in Fresh Jos Attack (Video)

-

Politics2 days ago

Politics2 days agoOnyejeocha resigns as Minister of State for Labour

-

News18 hours ago

News18 hours agoKaduna Mando Garage Explosion Not Bomb- Police

-

Politics2 days ago

Politics2 days agoLabour Party to hold presidential primary April 28

-

Politics2 days ago

Politics2 days agoNo force can defeat Tinubu in 2027 –Umahi

-

News18 hours ago

News18 hours agoAtiku hires US lobbying firm for $1.2m to boost image – Report

-

News2 days ago

News2 days agoJUST IN: Lagos Fire Service Successfully Contains Two Overnight Fire Incidents iin Lagos

-

News2 days ago

News2 days agoNigerian Army Debunks Claims of Attack on Bishop Matthew Kukah’s Residence and Sokoto Catholic Cathedral