News

Understanding Mortgage Options in Nigeria’s Real Estate Market by Dennis Isong

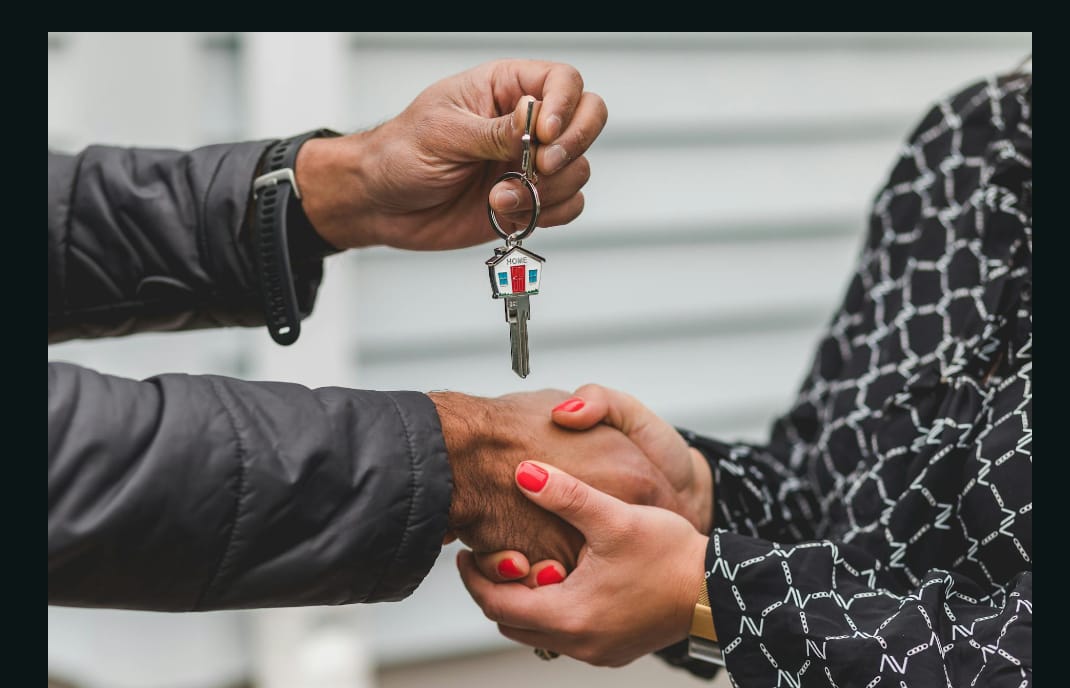

For Nigerians considering a mortgage, thorough research and preparation are essential.

As more Nigerians aspire to become homeowners, understanding the available mortgage options becomes essential.

This article discusses mortgage financing in Nigeria, exploring the various options available to prospective homeowners and investors..

The Nigerian MortgageNigeria’s mortgage industry, while still developing, has made considerable strides in recent years.

The Federal Mortgage Bank of Nigeria (FMBN) and the Nigeria Mortgage Refinance Company (NMRC) play pivotal roles in shaping the mortgage sector.

These institutions work alongside commercial banks and primary mortgage banks to provide various mortgage products to Nigerians.

The mortgage-to-GDP ratio in Nigeria remains relatively low compared to more developed economies, indicating significant room for growth.

However, challenges such as high interest rates, limited long-term funding, and stringent lending criteria have historically hindered widespread mortgage adoption.

Despite these obstacles, recent government initiatives and private sector innovations are gradually making mortgages more accessible to a broader segment of the population.

Types of Mortgage Options

Nigerian homebuyers and investors can choose from several mortgage options, each with its unique features and requirements.

The most common types include:Federal Mortgage Bank of Nigeria (FMBN) Loans:

These are government-backed mortgages designed to provide affordable housing finance to Nigerian workers.

The National Housing Fund (NHF) scheme, administered by the FMBN, allows contributors to access loans at favorable interest rates for home purchase or construction.

Commercial Bank Mortgages: Many commercial banks in Nigeria offer mortgage products to their customers.

These loans typically have higher interest rates compared to government-backed options but may offer more flexibility in terms of loan amounts and repayment periods.

Primary Mortgage Bank Loans: Specialized mortgage institutions provide various home financing options, often with more competitive rates than commercial banks.

These institutions focus exclusively on mortgage lending and may offer more tailored products to meet specific needs.

Rent-to-Own Schemes: Some developers and financial institutions offer rent-to-own arrangements, allowing tenants to gradually build equity in a property while paying rent.

This option can be particularly attractive for those who may not qualify for traditional mortgages.

Cooperative Society Loans: Many Nigerians participate in cooperative societies that pool resources to provide housing loans to members.

These loans often come with lower interest rates and more flexible terms compared to traditional banking options.Eligibility and Requirements

Securing a mortgage in Nigeria typically requires meeting certain eligibility criteria and fulfilling specific requirements. While these may vary depending on the lender and the type of mortgage, common factors include:

Income and Employment:

Lenders generally require proof of stable income and employment. The debt-to-income ratio is a crucial factor in determining loan eligibility and amount.Credit History:

Although Nigeria lacks a comprehensive credit scoring system, lenders may review an applicant’s credit history and repayment record on previous loans.

Down Payment: Most mortgage options in Nigeria require a significant down payment, typically ranging from 20% to 30% of the property’s value.

Some government-backed schemes may offer lower down payment requirements.Property Valuation: The property being purchased or used as collateral must undergo a professional valuation to determine its market value and ensure it meets the lender’s criteria.

Documentation: Applicants must provide various documents, including identification, proof of income, tax clearance certificates, and property-related documents.

Age Limit: Many lenders impose age restrictions, often requiring the mortgage to be fully repaid before the borrower reaches retirement age.

Challenges and Opportunities in Nigerian Mortgage Financing.

While the Nigerian mortgage market continues to evolve, several challenges persist. High interest rates, often in double digits, make mortgages unaffordable for many Nigerians.

The lack of long-term funding sources limits the ability of lenders to offer extended repayment periods, which could make monthly payments more manageable.Land tenure issues and the complexities of property registration in some parts of the country also pose significant hurdles.

The time and cost associated with perfecting property titles can add to the overall expense of obtaining a mortgage.

However, these challenges also present opportunities for innovation in the mortgage sector. Fintech companies are entering the market with digital solutions that streamline the mortgage application and approval process.

Some lenders are exploring alternative credit scoring methods to assess creditworthiness, potentially opening up mortgage access to a broader population.

The government’s ongoing efforts to address housing deficits through initiatives like the Family Homes Fund and the National Housing Programme are creating new opportunities for affordable mortgage financing.

Additionally, the gradual development of the secondary mortgage market through the Nigeria Mortgage Refinance Company (NMRC) is expected to increase liquidity in the sector and potentially lead to more competitive mortgage rates.

Navigating the Mortgage Process.

For Nigerians considering a mortgage, thorough research and preparation are essential.

Prospective borrowers should:

● Compare offerings from multiple lenders to find the best rates and terms.

● Understand all associated costs, including processing fees, insurance, and potential penalties for early repayment.

● Seek professional advice from financial advisors or real estate experts to make informed decisions.

● Consider the long-term implications of the mortgage, including how it aligns with future financial goals and career plans.

● Stay informed about government policies and initiatives that may affect the mortgage market or provide new opportunities for home financing.

As Nigeria’s real estate market continues to grow and evolve, so too will the mortgage options available to its citizens.

By understanding the current landscape and staying informed about new developments, prospective homeowners and investors can make the most of the opportunities presented by mortgage financing in Nigeria’s dynamic real estate sector.

For personalized assistance with your property needs, contact Dennis Isong, a top Lagos realtor specializing in helping Nigerians in the diaspora own property stress-free.Contact: +2348164741041

News

Police must pay transport fares, says AIG

” No police officer has the right to enter your vehicle without paying. We should assist one another willingly, not by force,” he said.

• The Assistant Inspector-General of Police(AIG) in charge of Zone 2 Command, Mr Olohundare Jimoh, speaking with transporters at Obalende garage, Lagos State, on Wednesday.

The Assistant Inspector-General of Police, Zone 2 Command, Mr Olohundare Jimoh, has declared that officers must pay fares before boarding commercial vehicles, warning against abuse of authority.

Jimoh spoke on Wednesday at Obalende garage during a sensitisation meeting with drivers and transport workers marking National Police Day 2026.

He stressed that relations between police and the public must be based on partnership, not coercion, urging both sides to support each other voluntarily.

“No police officer has the right to enter your vehicle without paying. We should assist one another willingly, not by force,” he said.

Jimoh called for stronger cooperation to maintain safety and order on roads, insisting there was no conflict between officers and transport unions.

“I don’t collect money from officers. We don’t arrest people arbitrarily. If you have issues with any officer, report directly to me,” he said.

(Vanguard)

President Bola Ahmed Tinubu will leave for Jos tomorrow to commiserate with the state government and residents over recent deadly gun attacks that lefts dozens dead.

This was following Governor Caleb Mutfwang’s security briefing to the President on the recent violent attack in Angwan Rukuba, Plateau State.

During the meeting on Wednesday at the presidential villa in Abuja, Governor Caleb Mutfwang told Mr President that although security forces have restored calm after fresh disturbances involving looters on Wednesday morning, following the deadly Palm Sunday attack that left more than a dozen dead and many others injured.

He said that investigations are continuing to determine the identities or motives of the attackers who are yet to be apprehended .

Presidency source said that President Tinubu was initially scheduled for a planned trip to Ogun State to flag off operations at the Gateway International Cargo Airport on Thursday.

From Jos, the President will travel to Lagos to observe Good Friday.

On Saturday, April 4, he will visit Ogun State to commission projects including the cargo airport.

He will then return to Lagos during the Easter holiday to commission several state infrastructure projects, including the Ojota/Opebi Link Bridge.

Before heading back to Abuja, the president will visit Bayelsa State on April 10 to commission projects completed under Governor Duoye Diri.

President Bola Ahmed Tinubu will tomorrow embark on a visit to Jos, Plateau State, as the first leg of a five-state tour across the country.

The Presidency announced that the President has postponed his scheduled trip to Ogun State to enable him to commence the series of official visits.

Details of the remaining four states in the tour are expected to be released by the Presidency in due course.

The development comes as President Tinubu continues nationwide engagements aimed at assessing development projects, interacting with stakeholders, and addressing key national issues in the respective states.

Further updates on the itinerary will be communicated as the visits progress.

INEC Dismisses Calls for Chairman’s Removal

Ebonyi: Gunmen Assasinate Another Traditional Ruler

From South Africa to US, ‘Cicada’ COVID-19 variant spreading

Tech Expert, Zuckerberg trains with UFC champions, Adesanya, Alexander

Organ Trafficking: Ekweremadu bags 10 years in UK prison

SAINT OBI: Between his marriage and his death

-

Business2 days ago

Business2 days ago33 Nigerian Banks Beat CBN’s Recapialisation with ₦4.65trn Combined Capital Base

-

Politics2 days ago

Politics2 days agoBREAKING: INEC Withdraws Recognition of David Mark’s ADC

-

Sports2 days ago

Sports2 days agoFirstBank Sponsors Samuel Okwaraji U-16 Football Championship 2026

-

News2 days ago

News2 days agoJUST IN: Tinubu Heads to Jos Tomorrow, Postpones Ogun Trip for 5-State Visits

-

News2 days ago

News2 days agoEaster: FG declares Friday, Monday public holidays

-

Entertainment2 days ago

Entertainment2 days agoSuper Eagles Iwobi to launch music album ‘More To Life’

-

News2 days ago

News2 days agoGas Leak in Ogun School: 30 Students, Teacher Hospitalised

-

Politics2 days ago

Politics2 days agoArise News Anchor Ikokwu in Political Race for Reps Seat