Business

Nigeria’s economy may be back from the brink — The Economist

Improvements in macroeconomic stability are restoring investor confidence.

• President Bola Tinubu

A spate of painful reforms is beginning to show results.

When nigeria returned to civilian rule in 1999, Olusegun Obasanjo, the elected president, set out to clean up the economy after years of mismanagement by military governments.

Initially dismissed by critics, by the end of his second term Mr Obasanjo’s liberal policies had tamed inflation, spurred investment and raised annual gdp growth to around 7 percent.

It didn’t last. Over the past decade gdp per person has fallen.

Yet evidence is now mounting that another stretch of “golden years”, as one analyst calls the period following Mr Obasanjo’s liberalisation, may be on the cards.

In the past two and a half years Bola Tinubu, who in Mr Obasanjo’s day was the governor of Lagos and was elected president in 2023, has been enacting his own set of structural reforms.

As he gears up to run for a second term in 2027, they may be starting to pay off.

It is difficult to overstate the mess Mr Tinubu inherited.

When he took office in 2023, the country’s central bank had $7 billion (equivalent to 1.4% of gdp at the time) in obligations it could not meet, prompting international investors to flee en masse.

The bank’s credibility had been dented by a recklessly loose monetary policy, its mismanagement of dwindling foreign-exchange reserves and efforts to maintain an unsustainable tiered exchange-rate system.

Poverty has risen. But it looks as though Mr Tinubu’s bitter medicine is helping.

In 2022 alone the cash-strapped government spent some $10 billion, equivalent to 2.2% of gdp, on a ruinous fuel subsidy.

To fix things, Mr Tinubu’s government got on with a package of drastic structural reforms. It abolished the fuel subsidy and abandoned that multi-tiered system of dollar-pegged exchange rates, largely allowing the naira to float.

The Central Bank aggressively tightened monetary policy to curb the resulting bout of inflation.

The government also moved to improve security in the Niger Delta and offered a range of tax incentives to investors to boost dwindling oil production.

Nearly three years on, Nigeria’s 230 million people, especially the poor and the middle class, are still reeling from increases in fuel and food prices.

Poverty has risen. But it looks as though Mr Tinubu’s bitter medicine is helping.

The annual inflation rate, which hit a nearly 30-year high of 34.8% in December 2024, fell to 15.2% in December 2025.

Growth is returning.

The IMF expects the economy to expand by 4.4% in 2026.

Following two steep devaluations in 2023, the naira has stabilised (see chart).

The Central Bank’s foreign-exchange reserves have risen to $46 billion, their highest level in seven years.

Improvements in macroeconomic stability are restoring investor confidence.

On January 22nd Shell, a British company, said it hopes in 2027 to finalise plans, with partners, to develop a $20 billion offshore oilfield that has been sitting untapped for over 20 years.

Exxon Mobil, an American firm, has committed $1.5 billion to deep water development until 2027.

Local business leaders are more upbeat, too.

Oil-and-gas production is rising, much of it driven by local firms plugging leaks and improving output in onshore projects in the Niger Delta, which has become safer thanks to Mr Tinubu’s focus on security there.

All this should give the government some fiscal breathing room, particularly as the cheaper naira begins to raise the competitiveness of Nigeria’s non-oil exports such as cocoa and cashew nuts.

Recent reforms to taxation and tax collection, Mr Tinubu’s latest project, should help improve revenues further in the coming years.

Falling inflation should eventually begin to ease the cost-of-living pain.

However, even optimists have plenty of reasons to be cautious.

Savings from the fuel subsidy have largely been spent on servicing the public debt, which is still rising as the government continues to borrow against future sales of oil to fund its deficit.

Currently, some 60% of revenues are consumed by debt service.

On January 20th Nigeria’s finance minister said the government hoped to borrow less this year, but current budget projections suggest that is not realistic.

“The government is broke.

There’s nothing to invest in the future, that’s the truth,” says Esili Eigbe of Escap, a Nigerian consultancy.

Unless the government cuts civil-service salaries, another big chunk of spending, or is able to restructure loans to make them cheaper, the extra revenue from recent tax reforms looks unlikely to be available for improving infrastructure or to pay for public health care and education.

“They’ve brought the deficit down, but they don’t seem to show any greater ability to get capital projects out of the door,“ says David Cowan, an economist at Citi, an American bank.

All this means that it will take a long time for ordinary Nigerians, who until now have mostly borne the pain of Mr Tinubu’s reforms, to feel any benefit.

Buying food has been a particular struggle, not just for the 42% of Nigerians who live on less than $3 a day, the World Bank’s definition of extreme poverty, but also for the urban middle class.

The price of a kilo of rice has nearly quadrupled since May 2023, while wages have barely budged.

Even though inflation is now falling, many still struggle to afford enough to eat.

Mr Obasanjo’s reforms in the early 2000s aimed to increase economic dynamism and improve people’s lives by attracting fresh capital investment into newly privatised sectors.

By the end of his second term in 2007, domestic companies were worth $85 billion, up from $3 billion in 1999.

Mr Tinubu, by contrast, has so far focused on restoring stability and reviving the country’s ailing oil-and-gas sector. To bring about more golden years for Nigerians, he needs to go beyond that. ■

Credit: The Economist

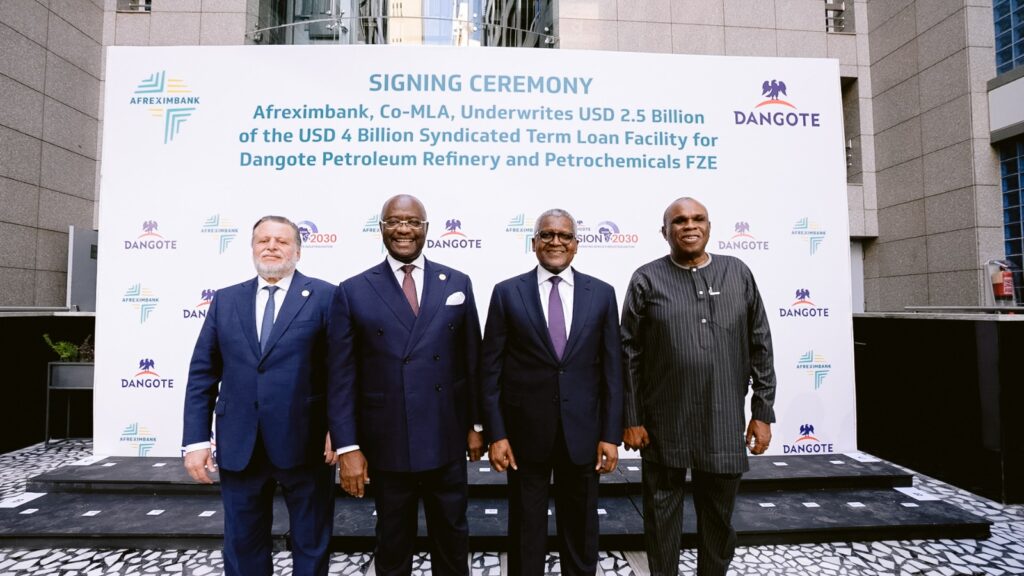

African Export-Import Bank has underwritten $2.5 billion in a $4 billion senior syndicated term loan for Dangote Petroleum Refinery and Petrochemicals, in a move aimed at strengthening the refinery’s financial position and supporting its long-term growth and expansion strategy.

The five-year facility, arranged alongside Access Bank as co-Mandated Lead Arrangers, is designed to consolidate existing debt, optimise the refinery’s capital structure and align its financing with current operational realities.

The transaction marks a significant milestone for the Dangote Refinery, Africa’s largest refining and petrochemical complex with a capacity of 650,000 barrels per day.

Afreximbank’s $2.5 billion participation represents the largest share of the syndicate, underscoring its strategic role in mobilising capital for industrial projects across the continent.

The bank said the financing aligns with its mandate to promote industrialisation, reduce reliance on imported petroleum products and deepen intra-African trade.

Since refining operations commenced in February 2024, Afreximbank has played a key role in supporting the project, including providing a $1 billion working capital facility and acting as financial adviser on the Naira-for-Crude initiative, which facilitates crude procurement and product sales in local currency.

Speaking during a strategy session in Cairo, Egypt, President and Chairman of the Board of Directors of Afreximbank, George Elombi, said the bank’s continued backing reflects confidence in indigenous African enterprises.

“We take immense pride in being the single largest provider of financing to the Dangote Group. We do so primarily because Dangote is African,” he said.

“When we invest in ourselves, we do more than create jobs and wealth or expand government revenues; we build a secure and resilient future for our continent”

Elombi disclosed that Afreximbank has committed about $15 billion to Dangote Group since 2015, highlighting the scale of its long-term partnership with the conglomerate.

President and Chief Executive of Dangote Industries Limited, Aliko Dangote, described the financing as a critical step in positioning the refinery for its next phase of expansion.

“This financing marks an important step in strengthening the financial foundation of Dangote Petroleum Refinery & Petrochemicals and positions the business for the next phase of its growth,” he said.

“We appreciate Afreximbank’s continued support and confidence in our vision to build world-class industrial capacity that serves Nigeria, Africa and global markets.”

The syndicated loan attracted strong participation from a mix of African and international financial institutions, reflecting sustained investor confidence in the refinery as a transformative industrial asset in advancing Africa’s energy security, reducing import dependence and supporting the continent’s broader industrialisation agenda.

Business

BUA Foods Plc Reports Strong 2025 Performance with ₦1.77 Trillion Revenue, Proposes Record ₦28 Dividend per Share

Leading Nigerian food manufacturer BUA Foods Plc has announced robust full-year 2025 audited results, with revenue climbing 16% to ₦1.77 trillion from ₦1.53 trillion in 2024.

The growth was driven by sustained consumer demand for the company’s core staples sugar, flour, pasta, and rice alongside higher sales volumes and strategic pricing amid a challenging economic environment marked by inflationary pressures on households.

Profit after tax nearly doubled, rising 95% to ₦518.4 billion, while gross profit surged to ₦737.3 billion from ₦540.8 billion the previous year.

Operating profit also increased significantly to ₦656.6 billion.In a strong signal of confidence in its outlook and commitment to shareholder value, the Board of Directors has proposed a final dividend of ₦28 per ordinary share of 50 kobo.

This represents a 115% increase from the ₦13 per share paid in 2024, translating to a total payout of approximately ₦504 billion, subject to approval by shareholders at the company’s 2026 Annual General Meeting.

Chairman Abdul Samad Rabiu highlighted the results, stating that the substantial dividend hike underscores the company’s dedication to rewarding investors while continuing to invest in business expansion and operational efficiency.

BUA Foods, a major player in Nigeria’s food processing sector controlled by billionaire Abdul Samad Rabiu, has continued to benefit from scale advantages, market expansion, and resilient demand for essential food products despite broader economic headwinds.

The company’s shares have reacted positively in recent trading, reflecting investor optimism over the strong earnings and generous dividend proposal.

Full details of the financial statements were filed with the Nigerian Exchange (NGX) on Monday.

Analysts view the performance as a testament to BUA Foods’ robust business model and ability to navigate Nigeria’s macroeconomic challenges through volume growth and cost discipline.

Business

OPay launches new office in Jos

” Opening this office in Jos allows us to stay closer to the people we serve, better understand their needs, and continue to provide fast, secure, and reliable financial services that improve everyday life.”

OPay has officially launched its new office in Jos, Plateau State.

Speaking at the event, OPay’s Chief Operations and Technology Officer, Dotun Adekunle, said that the new Jos office reflects OPay’s continued commitment to putting customers first and advancing financial inclusion across Nigeria.

He said :” Our customers are at the center of everything we do.

Opening this office in Jos allows us to stay closer to the people we serve, better understand their needs, and continue to provide fast, secure, and reliable financial services that improve everyday life.”

Afreximbank Leads $4bn Financing for Dangote Refinery with $2.5bn Commitment

JUST IN: El-Rufai Leaves State High Court for Federal High Court in Kaduna

El-Rufai Appear in State High Court, after Mother’s death, as Trial Continues

Tech Expert, Zuckerberg trains with UFC champions, Adesanya, Alexander

Organ Trafficking: Ekweremadu bags 10 years in UK prison

SAINT OBI: Between his marriage and his death

-

Sports3 days ago

Sports3 days agoCAF appoints Nigeria’s Samson Adamu as acting secretary general

-

Business3 days ago

Business3 days agoGovernor Otti Commissions Ultimum Manufacturing Plant in Aba

-

News2 days ago

News2 days agoPresident Tinubu at 74, Donates Salaries to Armed Forces Welfare Fund

-

Politics2 days ago

Politics2 days agoPDP will contest 2027 polls, says Wike

-

Politics2 days ago

Politics2 days agoPDP Leadership Crisis: Faction Heads to Supreme Court as Tussle Deepens

-

Business21 hours ago

Business21 hours agoBUA Foods Plc Reports Strong 2025 Performance with ₦1.77 Trillion Revenue, Proposes Record ₦28 Dividend per Share

-

Business2 days ago

Business2 days agoOPay launches new office in Jos

-

News21 hours ago

News21 hours agoNELFUND Debunks Claims of ₦25,000 Student Upkeep Allowance