Business

General Hydrocarbons Limited Vs FBN: The Explainer GHL vs FBN: The Facts, The Half-Truths and The Fiction

GHL will continue to fight for justice and damages whilst it remains open for mediation and resolution

1. Is GHL’s liability to First Bank a loan? The simple answer is NO, as it is not a normal commercial loan: it is a Project Finance relationship.

Here is how:

2. GHL is the awardee and licenced operator of OML 120. FBN approached GHL to finance the exploration, development and production of OML 120and share profit 50:50, while paying FBN cost of finance.

The FBN 50% share is dedicated to paydown its non-performing loan of $600million(discounted from $718million from AMCON’s Eligible Bank Asset) in order to resolve FBN’s solvency issues.In doing that, GHL guaranteed FBN’s liability to AMCON, through a Tripartite Agreement between GHL, FBN and AMCON.

3. The result of the Tripartite Agreement was that FBN became immediately profitable and moved from a loss of N302Billion to a profit of N151Bn for 2021 FYE. However, in return, it has failed to meet its commitment under the Tripartite Agreement to fully finance and make the payments required for the optimal exploration and development of OML 120 as agreed in the Tripartite Agreement, resulting in losses in day rates and downtimes of $47million, which has snowballed into the current impasseas FBN has failed to make further required payments for the drilling and exploration of OML 120. Essentially, FBN failed to fulfil its condition precedent to profitability in failing to finance OML 120 as agreed, leavingits financial statements open to challenge. Meanwhile the FBN’s claim of $225Million loan is not due as it is still covered by moratorium, given that the project has not achieved commercial production. So, at best FBN’sclaim is premature.

4. GHL has now gone for Arbitration which is ongoing and FBN has gone to court with a series of Exparte (temporary) Mareva measures, the first of which has been vacated and the case is now being heard on the merit, whilst the second temporary Mareva is pending at the Federal High Court in Port-Harcourt, Rivers State, both supported by” wild, unfounded and unproven allegations of dissipation of assets.”

5. Did GHL dissipate any asset? The answer is no as all payments were made by First Bank DIRECTLY to 3rd parties after due diligence and verifications by FBN, and the 3rd parties are mainly global, world class, reputable companies with strict compliance regimes.

6. GHL is filing a claim of over $1Billion in various courts, while FBN is claiming $225million debt which it never complied with in line with the agreements.

GHL will continue to fight for justice and damages whilst it remains open for mediation and resolution.

Business

33 Nigerian Banks Beat CBN’s Recapialisation with ₦4.65trn Combined Capital Base

The recapitalisation programme has strengthened the capital base of Nigerian banks, reinforcing the resilience of the financial system and ensuring it is wellpositioned to support economic growth and withstand domestic and external shocks.”

•Governor of CBN, Olayemi Cardoso

The Central Bank of Nigeria (CBN) has wrapped up the banking sector recapitalisation programme it introduced two years ago (March 2024-March 31, 2026) with 33 banks successfully met the requirements deadline.

The banks raised a total of ₦4.65 trillion in new capital, according to a statement signed by Olubukola A. Akinwunmi, the Director, Banking Supervision and Hakama Sidi Ali (Mrs.), the Ag. Director, Corporate Communications.

It said that the recapialisation exercises recorded strong participation from both domestic and international investors, with 72.55% of capital sourced locally and 27.45% from international markets, reflecting sustained confidence in the Nigerian banking sector.

The statement noted that the Governor of CBN, Olayemi Cardoso said “the recapitalisation programme has strengthened the capital base of Nigerian banks, reinforcing the resilience of the financial system and ensuring it is wellpositioned to support economic growth and withstand domestic and external shocks.”

“The CBN confirms that 33 banks have met the revised minimum capital requirements established under the programme.

A limited number of institutions remain subject to ongoing regulatory and judicial processes, which are being addressed through established supervisory and legal frameworks.

“All banks remain fully operational, ensuring continued access to banking services for customers.

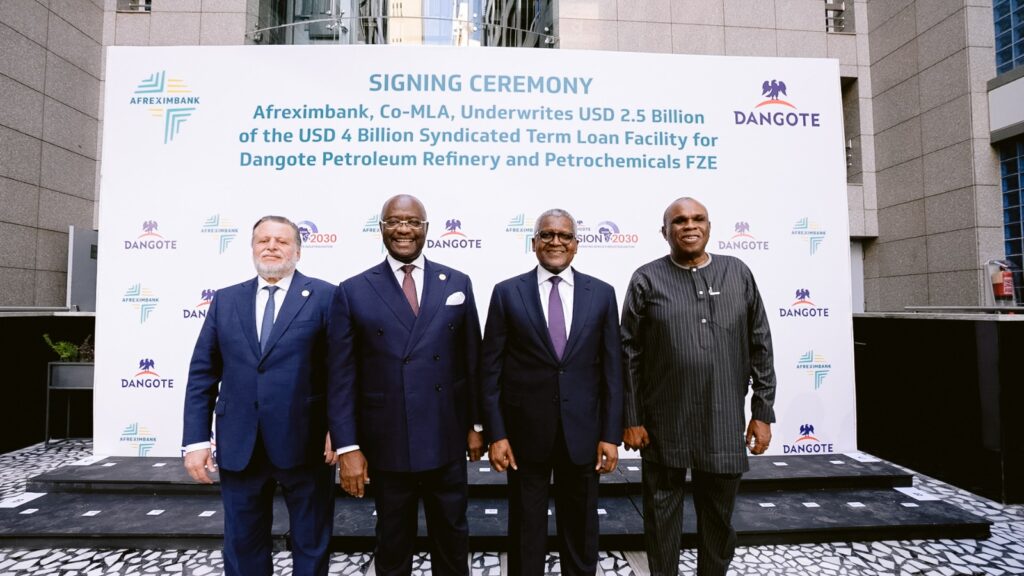

African Export-Import Bank has underwritten $2.5 billion in a $4 billion senior syndicated term loan for Dangote Petroleum Refinery and Petrochemicals, in a move aimed at strengthening the refinery’s financial position and supporting its long-term growth and expansion strategy.

The five-year facility, arranged alongside Access Bank as co-Mandated Lead Arrangers, is designed to consolidate existing debt, optimise the refinery’s capital structure and align its financing with current operational realities.

The transaction marks a significant milestone for the Dangote Refinery, Africa’s largest refining and petrochemical complex with a capacity of 650,000 barrels per day.

Afreximbank’s $2.5 billion participation represents the largest share of the syndicate, underscoring its strategic role in mobilising capital for industrial projects across the continent.

The bank said the financing aligns with its mandate to promote industrialisation, reduce reliance on imported petroleum products and deepen intra-African trade.

Since refining operations commenced in February 2024, Afreximbank has played a key role in supporting the project, including providing a $1 billion working capital facility and acting as financial adviser on the Naira-for-Crude initiative, which facilitates crude procurement and product sales in local currency.

Speaking during a strategy session in Cairo, Egypt, President and Chairman of the Board of Directors of Afreximbank, George Elombi, said the bank’s continued backing reflects confidence in indigenous African enterprises.

“We take immense pride in being the single largest provider of financing to the Dangote Group. We do so primarily because Dangote is African,” he said.

“When we invest in ourselves, we do more than create jobs and wealth or expand government revenues; we build a secure and resilient future for our continent”

Elombi disclosed that Afreximbank has committed about $15 billion to Dangote Group since 2015, highlighting the scale of its long-term partnership with the conglomerate.

President and Chief Executive of Dangote Industries Limited, Aliko Dangote, described the financing as a critical step in positioning the refinery for its next phase of expansion.

“This financing marks an important step in strengthening the financial foundation of Dangote Petroleum Refinery & Petrochemicals and positions the business for the next phase of its growth,” he said.

“We appreciate Afreximbank’s continued support and confidence in our vision to build world-class industrial capacity that serves Nigeria, Africa and global markets.”

The syndicated loan attracted strong participation from a mix of African and international financial institutions, reflecting sustained investor confidence in the refinery as a transformative industrial asset in advancing Africa’s energy security, reducing import dependence and supporting the continent’s broader industrialisation agenda.

Business

BUA Foods Plc Reports Strong 2025 Performance with ₦1.77 Trillion Revenue, Proposes Record ₦28 Dividend per Share

Leading Nigerian food manufacturer BUA Foods Plc has announced robust full-year 2025 audited results, with revenue climbing 16% to ₦1.77 trillion from ₦1.53 trillion in 2024.

The growth was driven by sustained consumer demand for the company’s core staples sugar, flour, pasta, and rice alongside higher sales volumes and strategic pricing amid a challenging economic environment marked by inflationary pressures on households.

Profit after tax nearly doubled, rising 95% to ₦518.4 billion, while gross profit surged to ₦737.3 billion from ₦540.8 billion the previous year.

Operating profit also increased significantly to ₦656.6 billion.In a strong signal of confidence in its outlook and commitment to shareholder value, the Board of Directors has proposed a final dividend of ₦28 per ordinary share of 50 kobo.

This represents a 115% increase from the ₦13 per share paid in 2024, translating to a total payout of approximately ₦504 billion, subject to approval by shareholders at the company’s 2026 Annual General Meeting.

Chairman Abdul Samad Rabiu highlighted the results, stating that the substantial dividend hike underscores the company’s dedication to rewarding investors while continuing to invest in business expansion and operational efficiency.

BUA Foods, a major player in Nigeria’s food processing sector controlled by billionaire Abdul Samad Rabiu, has continued to benefit from scale advantages, market expansion, and resilient demand for essential food products despite broader economic headwinds.

The company’s shares have reacted positively in recent trading, reflecting investor optimism over the strong earnings and generous dividend proposal.

Full details of the financial statements were filed with the Nigerian Exchange (NGX) on Monday.

Analysts view the performance as a testament to BUA Foods’ robust business model and ability to navigate Nigeria’s macroeconomic challenges through volume growth and cost discipline.

Onyejeocha resigns as Minister of State for Labour

No force can defeat Tinubu in 2027 –Umahi

Labour Party to hold presidential primary April 28

Tech Expert, Zuckerberg trains with UFC champions, Adesanya, Alexander

Organ Trafficking: Ekweremadu bags 10 years in UK prison

SAINT OBI: Between his marriage and his death

-

Business3 days ago

Business3 days ago33 Nigerian Banks Beat CBN’s Recapialisation with ₦4.65trn Combined Capital Base

-

Sports3 days ago

Sports3 days agoFirstBank Sponsors Samuel Okwaraji U-16 Football Championship 2026

-

Politics3 days ago

Politics3 days agoBREAKING: INEC Withdraws Recognition of David Mark’s ADC

-

News3 days ago

News3 days agoEaster: FG declares Friday, Monday public holidays

-

News3 days ago

News3 days agoJUST IN: Tinubu Heads to Jos Tomorrow, Postpones Ogun Trip for 5-State Visits

-

Entertainment3 days ago

Entertainment3 days agoSuper Eagles Iwobi to launch music album ‘More To Life’

-

News3 days ago

News3 days agoGas Leak in Ogun School: 30 Students, Teacher Hospitalised

-

Crime3 days ago

Crime3 days agoEl-Rufai Arrives Kaduna Court For Bail Hearing