News

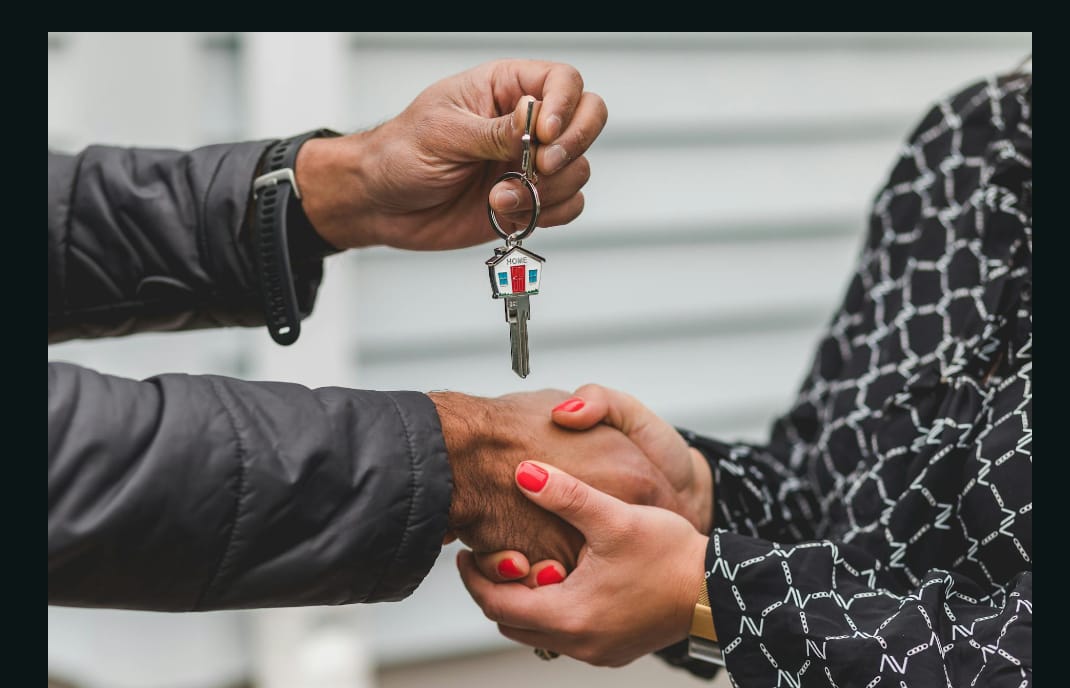

Understanding Mortgage Options in Nigeria’s Real Estate Market by Dennis Isong

For Nigerians considering a mortgage, thorough research and preparation are essential.

As more Nigerians aspire to become homeowners, understanding the available mortgage options becomes essential.

This article discusses mortgage financing in Nigeria, exploring the various options available to prospective homeowners and investors..

The Nigerian MortgageNigeria’s mortgage industry, while still developing, has made considerable strides in recent years.

The Federal Mortgage Bank of Nigeria (FMBN) and the Nigeria Mortgage Refinance Company (NMRC) play pivotal roles in shaping the mortgage sector.

These institutions work alongside commercial banks and primary mortgage banks to provide various mortgage products to Nigerians.

The mortgage-to-GDP ratio in Nigeria remains relatively low compared to more developed economies, indicating significant room for growth.

However, challenges such as high interest rates, limited long-term funding, and stringent lending criteria have historically hindered widespread mortgage adoption.

Despite these obstacles, recent government initiatives and private sector innovations are gradually making mortgages more accessible to a broader segment of the population.

Types of Mortgage Options

Nigerian homebuyers and investors can choose from several mortgage options, each with its unique features and requirements.

The most common types include:Federal Mortgage Bank of Nigeria (FMBN) Loans:

These are government-backed mortgages designed to provide affordable housing finance to Nigerian workers.

The National Housing Fund (NHF) scheme, administered by the FMBN, allows contributors to access loans at favorable interest rates for home purchase or construction.

Commercial Bank Mortgages: Many commercial banks in Nigeria offer mortgage products to their customers.

These loans typically have higher interest rates compared to government-backed options but may offer more flexibility in terms of loan amounts and repayment periods.

Primary Mortgage Bank Loans: Specialized mortgage institutions provide various home financing options, often with more competitive rates than commercial banks.

These institutions focus exclusively on mortgage lending and may offer more tailored products to meet specific needs.

Rent-to-Own Schemes: Some developers and financial institutions offer rent-to-own arrangements, allowing tenants to gradually build equity in a property while paying rent.

This option can be particularly attractive for those who may not qualify for traditional mortgages.

Cooperative Society Loans: Many Nigerians participate in cooperative societies that pool resources to provide housing loans to members.

These loans often come with lower interest rates and more flexible terms compared to traditional banking options.Eligibility and Requirements

Securing a mortgage in Nigeria typically requires meeting certain eligibility criteria and fulfilling specific requirements. While these may vary depending on the lender and the type of mortgage, common factors include:

Income and Employment:

Lenders generally require proof of stable income and employment. The debt-to-income ratio is a crucial factor in determining loan eligibility and amount.Credit History:

Although Nigeria lacks a comprehensive credit scoring system, lenders may review an applicant’s credit history and repayment record on previous loans.

Down Payment: Most mortgage options in Nigeria require a significant down payment, typically ranging from 20% to 30% of the property’s value.

Some government-backed schemes may offer lower down payment requirements.Property Valuation: The property being purchased or used as collateral must undergo a professional valuation to determine its market value and ensure it meets the lender’s criteria.

Documentation: Applicants must provide various documents, including identification, proof of income, tax clearance certificates, and property-related documents.

Age Limit: Many lenders impose age restrictions, often requiring the mortgage to be fully repaid before the borrower reaches retirement age.

Challenges and Opportunities in Nigerian Mortgage Financing.

While the Nigerian mortgage market continues to evolve, several challenges persist. High interest rates, often in double digits, make mortgages unaffordable for many Nigerians.

The lack of long-term funding sources limits the ability of lenders to offer extended repayment periods, which could make monthly payments more manageable.Land tenure issues and the complexities of property registration in some parts of the country also pose significant hurdles.

The time and cost associated with perfecting property titles can add to the overall expense of obtaining a mortgage.

However, these challenges also present opportunities for innovation in the mortgage sector. Fintech companies are entering the market with digital solutions that streamline the mortgage application and approval process.

Some lenders are exploring alternative credit scoring methods to assess creditworthiness, potentially opening up mortgage access to a broader population.

The government’s ongoing efforts to address housing deficits through initiatives like the Family Homes Fund and the National Housing Programme are creating new opportunities for affordable mortgage financing.

Additionally, the gradual development of the secondary mortgage market through the Nigeria Mortgage Refinance Company (NMRC) is expected to increase liquidity in the sector and potentially lead to more competitive mortgage rates.

Navigating the Mortgage Process.

For Nigerians considering a mortgage, thorough research and preparation are essential.

Prospective borrowers should:

● Compare offerings from multiple lenders to find the best rates and terms.

● Understand all associated costs, including processing fees, insurance, and potential penalties for early repayment.

● Seek professional advice from financial advisors or real estate experts to make informed decisions.

● Consider the long-term implications of the mortgage, including how it aligns with future financial goals and career plans.

● Stay informed about government policies and initiatives that may affect the mortgage market or provide new opportunities for home financing.

As Nigeria’s real estate market continues to grow and evolve, so too will the mortgage options available to its citizens.

By understanding the current landscape and staying informed about new developments, prospective homeowners and investors can make the most of the opportunities presented by mortgage financing in Nigeria’s dynamic real estate sector.

For personalized assistance with your property needs, contact Dennis Isong, a top Lagos realtor specializing in helping Nigerians in the diaspora own property stress-free.Contact: +2348164741041

News

A Review of Akwa Ibom State Government’s July Delivery Meeting

Stakeholders at the meeting delivered goodwill messages, commending Governor Umo Eno for institutionalising the Delivery Meeting as a platform for transparency, accountability, and inclusive governance.

Image: Governor Umo Eno

- The Akwa Ibom State Government’s Monthly Delivery Meeting concluded its two-day July session, with Governor Umo Eno presiding over an extensive review of the administration’s strategic projects across key sectors.

- Hon. Aniekan UmanahCommissioner for Information, reported that the meeting forms part of ongoing efforts to monitor implementation, evaluate progress, and ensure the timely delivery of projects under the ARISE Agenda.

- In his opening remarks on Day Two, Governor Eno reiterated that the Delivery Meeting has become a vital accountability mechanism for tracking the performance of government projects and ensuring that every initiative delivers measurable value to the people of the State.

- He stressed that the sessions provide an opportunity for honest appraisal, collective problem-solving, and improved coordination among implementing agencies as the administration continues to deliver on its commitments under the ARISE Agenda. Quoting the Greek philosopher Socrates, the Governor said, “An unexamined life is not worth living.”

- Before the commencement of the Day Two session, Governor Eno paid an unscheduled visit to the ARISE Palm Resort, an audacious tourism project built on a 73-hectare gully reclamation site, to verify claims made during the previous day’s presentations and assess firsthand the level of progress on the facility, which is scheduled for commissioning later in the year.

- The meeting received comprehensive presentations on key projects across multiple sectors of the state’s development programme, including agriculture, trade and investment, maritime and transportation, health, internal security, housing, tourism, local government administration, direct labour projects, and other flagship initiatives.

- Under the agricultural sector, presentations were made on the Ibom Model Farm, Agric Equipment Leasing Company, Distribution of Oil Palm Seedlings Programme, Dakkada Global Oil Palm Project, and the Akwa Ibom Agricultural Development Programme (AKADEP), with emphasis on mechanised farming, food security, and job creation.

- The Ministry of Trade and Investment presented updates on the International Market, Ikot Ekpene, highlighting its role in boosting commerce, attracting investment, and strengthening regional trade.

- The meeting noted the significant progress recorded on the project and urged the contractors to sustain the pace of work.

- In the maritime and transport sector, updates were presented on the Oron Maritime Infrastructure Project, which is aimed at improving maritime transportation, boosting commerce, and stimulating economic growth as part of the administration’s broader Blue Economy development initiatives.

- The health sector presentation covered the Ibom International Hospital, General Hospitals in Ukanafun, Ibiono Ibom, Ikot Ekpene, Iquita-Oron, Ikot Ekpene Udo, and other State of Emergency Health Projects, reinforcing the government’s commitment to providing accessible, affordable, and quality healthcare services.

- The Ministry of Internal Security and Waterways presented progress on the Counter Terrorism Unit Base, aimed at strengthening security infrastructure and enhancing public safety across the state.

- The Ministry of Housing provided updates on the Doctors’ Residence and the Executive and Legislative Quarters, projects aimed at providing decent accommodation while supporting urban renewal and improving living standards.

- In the tourism sector, progress on the Ibom International Hotel at the Convention Arena was reviewed, with emphasis on repositioning the facility to boost tourism, hospitality, and investment opportunities.

- Updates from the Ministry of Local Government and Chieftaincy Affairs covered the Chairmen’s Lodges, with an assurance that all 31 lodges will be completed by December 2026 to strengthen administrative efficiency at the grassroots level.

- The Direct Labour Committee reported progress on the Youth Development Centres, the One Project Per Local Government Area (Phase II), the Judiciary Village, and the House of Assembly Complex, all aimed at strengthening governance infrastructure and promoting youth development.

- Other strategic projects reviewed included the ARISE Shopping City, ARISE Park Beach Villas, AKBC Project, Model Secondary School, Senior Citizens Centre, and the Nigeria Formr Women Project, reflecting the administration’s broad development agenda across multiple sectors.

- Stakeholders at the meeting delivered goodwill messages, commending Governor Umo Eno for institutionalising the Delivery Meeting as a platform for transparency, accountability, and inclusive governance.

- Senator Effiong Bob commended the Governor for consistently engaging stakeholders in the governance process, noting that the ARISE Agenda is making measurable progress while praising the administration’s openness and transparency. Senior Advocate of Nigeria, Assam Assam, described the meeting as the most impactful yet, citing visible progress across sectors, particularly in healthcare infrastructure and service delivery.

- The Speaker of the Akwa Ibom State House of Assembly, Rt. Hon. Udeme Otong, lauded the Governor’s leadership and assured him of the continued support and collaboration of the State House of Assembly.

- The Oku Ibom Ibibio and President-General of the Supreme Council of Traditional Rulers, His Eminence, Ntenyin Dr. Solomon Etuk, JP, expressed pride in the administration’s developmental strides and commended Governor Eno’s inclusive approach to governance.

- In his closing remarks, Governor Umo Eno appreciated all participants, Heads of Ministries, Departments and Agencies (MDAs), Delivery Advisors, stakeholders, and contractors for their contributions to the two-day review exercise, noting that the sessions were rigorous but necessary in strengthening governance and ensuring accountability.

- The Governor stated that the administration is entering its “harvest season” as it gradually winds down its first term, adding that observations from the meeting would be used to further improve service delivery and implementation efficiency.

- He reaffirmed the government’s commitment to completing all ongoing projects within set timelines and urged implementing agencies to sustain the momentum and maintain high standards in project execution for the benefit of the people of Akwa Ibom State.

- At the conclusion of the Delivery Meeting, Governor Eno led stakeholders on an inspection visit to the Ibom Convention Arena to assess ongoing work on the 200-bed Ibom International Hotel project, which is billed for commissioning later in the year.

News

Explosion rocks Apapa tank farm; NPA, NIMASA move to curtail spread

Following the outbreak the fire service departments of both the Nigerian Ports Authority (NPA) and the Nigerian Maritime Administration and Safety Agency (NIMASA) moved in to curtail the spread of the inferno.

Panic erupted at the Lagos tank farm cluster at Ibafon, Apapa, on Friday morning after a fire broke out at the Bono Tank Farm, located within the Best Energy Tank Farm complex.

The inferno sent residents and workers in the area fleeing for safety as emergency responders moved in to contain the blaze.

Following the outbreak the fire service departments of both the Nigerian Ports Authority (NPA) and the Nigerian Maritime Administration and Safety Agency (NIMASA) moved in to curtail the spread of the inferno.

Efforts to obtain comments from the management of Bono Tank Farm and Best Energy Tank Farm were unsuccessful, as phone calls and text messages sent to their representatives were neither answered nor acknowledged.

News

FG slams 8-count charges on Adeyemi over fake agency ” I’m not a criminal”, he defends

It was learned that the alleged ‘‘fake’’ Presidential Economic Advisory Council/Presidential Foreign Intervention Promotion Council was allocated N1.302 billion in the 2026 Budget of the Federal Government.

Photo: Gbajabiamila, and Adeyemi

The Federal Government has filed an 8-count charges against Adeniyi Adeyemi, convener of a purported Presidential Foreign Intervention Promotion Council, PFIPC, over the controversy trailing the agency.

Adeyemi, however, fought back claiming that he was given an appointment letter.

Adeyemi, during an appearance on Channels Television claimed that the Chief of Staff to the President, Mr. Femi Gbajabiamila gave him an appointment letter, insisting that he is not a criminal.

However, it was learned that the alleged ‘‘fake’’ Presidential Economic Advisory Council/Presidential Foreign Intervention Promotion Council was allocated N1.302 billion in the 2026 Budget of the Federal Government.

In a statement on Wednesday, Bayo Onanuga, presidential spokesperson, said the charges were filed by the Police on November 27, 2025, against Adeyemi and two accomplices at the Federal High Court in Abuja.

Onanuga said Adeyemi is expected to appear in court on July 27, 2026.

A Review of Akwa Ibom State Government’s July Delivery Meeting

Explosion rocks Apapa tank farm; NPA, NIMASA move to curtail spread

FG slams 8-count charges on Adeyemi over fake agency ” I’m not a criminal”, he defends

Tech Expert, Zuckerberg trains with UFC champions, Adesanya, Alexander

Organ Trafficking: Ekweremadu bags 10 years in UK prison

SAINT OBI: Between his marriage and his death

-

Business2 days ago

Business2 days agoNaira Exchange Rates Thursday July 2, 2026

-

News2 days ago

News2 days agoFG Launches Digital Education Database, Seeks Full School Participation

-

News2 days ago

News2 days agoNIPSS: Gunmen attacks again, one killed

-

Business2 days ago

Business2 days agoIssue: Cloning Nigerian Investment Promotion Commission (NIPC)

-

News3 days ago

News3 days agoNigeria Moves from Decline to Stability – Finance Minister Oyedele (Photos)

-

Politics2 days ago

Politics2 days agoAtiku appoints Kenneth Okonkwo as spokesperson

-

News2 days ago

News2 days agoFG Hails End of Oyo Teacher’s Strike

-

Sports1 day ago

Sports1 day agoCape Verde faces defending world cup champions , Argentina today