Business

Fuel marketers kick as FG rules out price hike

Oil marketers, on Tuesday, advised President Bola Tinubu to gradually relax the removal of subsidy on Premium Motor Spirit, popularly called petrol, following the inability of importers to access the United States dollars and the impact which this was having on businesses.

This came as Tinubu ruled out fuel price hike and reversal of fuel subsidy.

However, marketers of petroleum products encouraged the President to learn from Kenya, stressing that the African country had to return subsidy on petrol to curb the devastating impact which its removal had on Kenyans.

“Let them not do the needful, they will see the consequences. We learned this morning that Kenya, which equally removed subsidy and noticed that its effect was so hard on the citizens, has again resumed the subsidy regime for the period of two months,” the Secretary, Independent Petroleum Marketers Association of Nigeria, Abuja-Suleja, Mohammed Shuaibu, told our correspondent.

He added, “Government is about the people and it must have a listening ear. For Nigeria, how can we be an oil producing nation with four refineries and all of them are down. We now depend on imports.

“When he (Tinubu) announced that thing (subsidy removal), we said it was going to bring problems. Are we not feeling the consequences of that announcement now? It is forex that largely determines the cost of petroleum products here.

“Marketers are not willing to import products again, So if the government is going to relax the removal of subsidy for a while, it should better do that as a matter of urgency.”

Shuaibu argued that despite the fact that the Nigerian National Petroleum Company Limited announced earlier on Tuesday that it had no intention of increasing petrol price, the cost of the commodity would rise above its current N617/litre in weeks, if the exchange rate continues to increase.

“Relaxing subsidy removal is going to be a very wise decision right now, because going by the price of the dollar, the cost of petrol is bound to rise. In fact, some oil marketers are ready to join the labour union to protest,” he added.

Some dealers had said subsidy on petrol would gradually creep in, should the NNPCL continue to sell at N617/litre, particularly if the rise in forex rate persists.

The National Public Relations Officer, Independent Petroleum Marketers Association of Nigeria, Chief Chinedu Ukadike, said the outright removal of subsidy would cause severe hardship.

“I’ve been saying this even before subsidy on petrol was removed. How can you stop subsidy without anything on ground as palliatives?

“Trips that used to be N5,000 in the past and now over N15,000. Businesses are shutting down. The suffering is rising. The government has to intervene now,” he stated.

The IPMAN PRO had earlier explained that the price of imported commodities, including petrol, would continue to rise as far as the rate of exchange of the dollar increases.

“Once there is a slack in the naira against the dollar, there is going to be an effect. The demand and supply of forex is a key factor. We should also understand that it is not only petroleum products that use forex.

NEITI reacts

This came as the Nigeria Extractive Industries Transparency Initiative advised the government to initiate and implement a deliberate policy that would attract investors to invest and help in fixing Nigeria’s refineries.

In its latest policy advisory for the oil sector, NEITI advised the Federal Government to come up with a deliberate policy to encourage private investments in refineries.

“A deliberate policy initiative should be implemented with full Presidential backing to encourage Nigerians and foreign investors already awarded licences to establish private refineries in Nigeria.

“The incentives may include tax holidays, institutional support, and availing potential investors in the downstream sector of the available opportunities within the existing ‘Federal Government ease of doing business policy.’

Also calling for intervention, the Executive Secretary, Major Oil Marketers Association of Nigeria, Clement Isong, earlier stated that it was high time the government intervened.

“Well, the President himself said in his speech that if they find petrol prices moving too high, they would intervene. We don’t want prices to move too high, nobody wants that.

“So if the dollar continues to climb, we are expecting some sort of intervention from the government based on what the President said,” the MOMAN official stated.

Similarly, the National President, Natural Oil and Gas Suppliers Association of Nigeria, Benneth Korie, told journalists that one of the best options before President Tinubu currently, was to hasten the repair of Nigeria’s refineries.

Tinubu reacts

Amidst the hike in cost of living brought about by the removal on Premium Motor Spirit popularly known has petrol which has led to a corresponding increase in fuel prices, the Presidency on Tuesday said Nigeria is currently the only country in West Africa enjoying the cheapest and most affordable price of PMS.

The Special Adviser to the President on Media and Publicity, Ajuri Ngelale, told State House correspondents that daily consumption of fuel has dropped from 67M litres to 46M litres following the removal of subsidy.

Ngelale, who noted that he spoke to the President on Tuesday morning, noted that the President urged stakeholders in the country to hold their peace while adding that the threats of an indefinite strike by the organized labour was premature.

He said, “The President wishes first to state that it is incumbent upon all stakeholders in the country to hold their peace. We have heard very recently from the organised labour movement in the country with respect to their most recent threat.

“We believe that the threat was premature and that there is a need on all sides to ensure that fact finding and diligence is done on what the current state of the downstream and midstream petroleum industry is before any threats or conclusions are arrived at or issued.Secondly, Mr. President, wishes to assure Nigerians following the announcement by the NNPC limited just yesterday that there will be no increase in the pump price of petroleum motor spirit anywhere in the country. We repeat, the president affirms that there will be no increase in the pump price of petroleum motor spirit.”

Speaking further, Ajuri noted that the market having been deregulated would no longer allow a single entity to dominate the market.

“The market has been deregulated. It has been liberalized and we are moving forward in that direction without looking back.

“The President also wishes to affirm that there are presently inefficiencies within the midstream and downstream petroleum sub sectors that once very swiftly addressed and cleaned up will ensure that we can maintain prices where they are without having to resort to a reversal of this administration’s deregulation policy in the petroleum industry.”

Ngelale also noted that Tinubu approved that the chart containing prices of PMS in other countries be transmitted to Nigerians so as to show the cost of PMS in West African countries.

He added, “Senegal at pump price today of N1,273 equivalent per liter, Guinea at N1,075 per liter, Côte d’ Ivore at N1,048 per litre equivalent in their currency, Mali N1,113 per litre, Central African Republic N1,414 per litre, Nigeria is presently averaging between N568 and N630 per litre.

“We are presently the cheapest, most affordable purchasing state in the West African sub-region by some distance. There is no country that is below N700 per liter.

Meanwhile, the Nigerian National Petroleum Corporation, in a post around 11.48pm on Monday on its official X (formerly Twitter) said it had no intention to increase the pump price of petrol.

Business

33 Nigerian Banks Beat CBN’s Recapialisation with ₦4.65trn Combined Capital Base

The recapitalisation programme has strengthened the capital base of Nigerian banks, reinforcing the resilience of the financial system and ensuring it is wellpositioned to support economic growth and withstand domestic and external shocks.”

•Governor of CBN, Olayemi Cardoso

The Central Bank of Nigeria (CBN) has wrapped up the banking sector recapitalisation programme it introduced two years ago (March 2024-March 31, 2026) with 33 banks successfully met the requirements deadline.

The banks raised a total of ₦4.65 trillion in new capital, according to a statement signed by Olubukola A. Akinwunmi, the Director, Banking Supervision and Hakama Sidi Ali (Mrs.), the Ag. Director, Corporate Communications.

It said that the recapialisation exercises recorded strong participation from both domestic and international investors, with 72.55% of capital sourced locally and 27.45% from international markets, reflecting sustained confidence in the Nigerian banking sector.

The statement noted that the Governor of CBN, Olayemi Cardoso said “the recapitalisation programme has strengthened the capital base of Nigerian banks, reinforcing the resilience of the financial system and ensuring it is wellpositioned to support economic growth and withstand domestic and external shocks.”

“The CBN confirms that 33 banks have met the revised minimum capital requirements established under the programme.

A limited number of institutions remain subject to ongoing regulatory and judicial processes, which are being addressed through established supervisory and legal frameworks.

“All banks remain fully operational, ensuring continued access to banking services for customers.

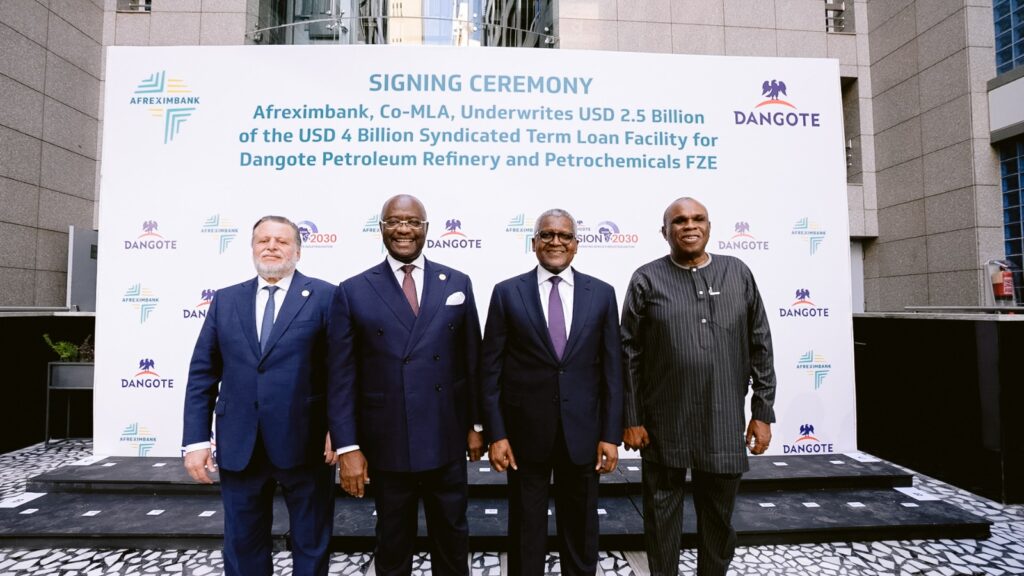

African Export-Import Bank has underwritten $2.5 billion in a $4 billion senior syndicated term loan for Dangote Petroleum Refinery and Petrochemicals, in a move aimed at strengthening the refinery’s financial position and supporting its long-term growth and expansion strategy.

The five-year facility, arranged alongside Access Bank as co-Mandated Lead Arrangers, is designed to consolidate existing debt, optimise the refinery’s capital structure and align its financing with current operational realities.

The transaction marks a significant milestone for the Dangote Refinery, Africa’s largest refining and petrochemical complex with a capacity of 650,000 barrels per day.

Afreximbank’s $2.5 billion participation represents the largest share of the syndicate, underscoring its strategic role in mobilising capital for industrial projects across the continent.

The bank said the financing aligns with its mandate to promote industrialisation, reduce reliance on imported petroleum products and deepen intra-African trade.

Since refining operations commenced in February 2024, Afreximbank has played a key role in supporting the project, including providing a $1 billion working capital facility and acting as financial adviser on the Naira-for-Crude initiative, which facilitates crude procurement and product sales in local currency.

Speaking during a strategy session in Cairo, Egypt, President and Chairman of the Board of Directors of Afreximbank, George Elombi, said the bank’s continued backing reflects confidence in indigenous African enterprises.

“We take immense pride in being the single largest provider of financing to the Dangote Group. We do so primarily because Dangote is African,” he said.

“When we invest in ourselves, we do more than create jobs and wealth or expand government revenues; we build a secure and resilient future for our continent”

Elombi disclosed that Afreximbank has committed about $15 billion to Dangote Group since 2015, highlighting the scale of its long-term partnership with the conglomerate.

President and Chief Executive of Dangote Industries Limited, Aliko Dangote, described the financing as a critical step in positioning the refinery for its next phase of expansion.

“This financing marks an important step in strengthening the financial foundation of Dangote Petroleum Refinery & Petrochemicals and positions the business for the next phase of its growth,” he said.

“We appreciate Afreximbank’s continued support and confidence in our vision to build world-class industrial capacity that serves Nigeria, Africa and global markets.”

The syndicated loan attracted strong participation from a mix of African and international financial institutions, reflecting sustained investor confidence in the refinery as a transformative industrial asset in advancing Africa’s energy security, reducing import dependence and supporting the continent’s broader industrialisation agenda.

Business

BUA Foods Plc Reports Strong 2025 Performance with ₦1.77 Trillion Revenue, Proposes Record ₦28 Dividend per Share

Leading Nigerian food manufacturer BUA Foods Plc has announced robust full-year 2025 audited results, with revenue climbing 16% to ₦1.77 trillion from ₦1.53 trillion in 2024.

The growth was driven by sustained consumer demand for the company’s core staples sugar, flour, pasta, and rice alongside higher sales volumes and strategic pricing amid a challenging economic environment marked by inflationary pressures on households.

Profit after tax nearly doubled, rising 95% to ₦518.4 billion, while gross profit surged to ₦737.3 billion from ₦540.8 billion the previous year.

Operating profit also increased significantly to ₦656.6 billion.In a strong signal of confidence in its outlook and commitment to shareholder value, the Board of Directors has proposed a final dividend of ₦28 per ordinary share of 50 kobo.

This represents a 115% increase from the ₦13 per share paid in 2024, translating to a total payout of approximately ₦504 billion, subject to approval by shareholders at the company’s 2026 Annual General Meeting.

Chairman Abdul Samad Rabiu highlighted the results, stating that the substantial dividend hike underscores the company’s dedication to rewarding investors while continuing to invest in business expansion and operational efficiency.

BUA Foods, a major player in Nigeria’s food processing sector controlled by billionaire Abdul Samad Rabiu, has continued to benefit from scale advantages, market expansion, and resilient demand for essential food products despite broader economic headwinds.

The company’s shares have reacted positively in recent trading, reflecting investor optimism over the strong earnings and generous dividend proposal.

Full details of the financial statements were filed with the Nigerian Exchange (NGX) on Monday.

Analysts view the performance as a testament to BUA Foods’ robust business model and ability to navigate Nigeria’s macroeconomic challenges through volume growth and cost discipline.

Ebonyi: Gunmen Assasinate Another Traditional Ruler

From South Africa to US, ‘Cicada’ COVID-19 variant spreading

FIFA ranks Super Eagles third in Africa, 26th globally

Tech Expert, Zuckerberg trains with UFC champions, Adesanya, Alexander

Organ Trafficking: Ekweremadu bags 10 years in UK prison

SAINT OBI: Between his marriage and his death

-

Business3 days ago

Business3 days agoBUA Foods Plc Reports Strong 2025 Performance with ₦1.77 Trillion Revenue, Proposes Record ₦28 Dividend per Share

-

News3 days ago

News3 days agoNELFUND Debunks Claims of ₦25,000 Student Upkeep Allowance

-

Business1 day ago

Business1 day ago33 Nigerian Banks Beat CBN’s Recapialisation with ₦4.65trn Combined Capital Base

-

News3 days ago

News3 days agoTinubu Appoints CAC, NPC, Officials, Names Adviser on Political Economy

-

Sports3 days ago

Sports3 days agoSportsville Awards: Olopade Leads NSC Delegation to Honour Dikko with Transformative Impact Award

-

News3 days ago

News3 days agoNigeria Welcomes African Games Bid Evaluation Committee

-

Sports1 day ago

Sports1 day agoFirstBank Sponsors Samuel Okwaraji U-16 Football Championship 2026

-

Politics1 day ago

Politics1 day agoBREAKING: INEC Withdraws Recognition of David Mark’s ADC