Business

Financial Inclusion: FG Engages ICAN, CIBN and four other Professional Bodies to Train 10 million Nigerians

Shettima noted that the nation “cannot build a one-trillion-dollar economy on weak skills, fragmented standards, or disconnected professional ecosystems.

• VP Shettima

The Federal Government, through the Office of the Vice President, has launched a nationwide training program to educate 10 million Nigerians on financial inclusion and literacy.

The training being implemented through the Presidential Committee on Economic & Financial Inclusion (PreCEFI), chaired by Vice President Kashim Shettima, is designed to equip Nigerians, particularly women and youths, with essential financial skills, investment knowledge, and digital competencies for sustainable wealth creation.

The Office of the Vice President, through the PreCEFI, on Monday, signed the Memorandum of Understanding (MOU) with the Institute of Chartered Accountants of Nigeria (ICAN); Chartered Institute of Bankers of Nigeria (CIBN); Chartered Institute of Stockbrokers (CIS); National Institute of Credit Administration (NICA); Chartered Risk Management Institute (CRMI) and Nigeria Institute of Innovation and Entrepreneurship (NIIE.

They are to jointly design training programmes, certification pathways, digital skills initiatives, and mentorship platforms that would strengthen Nigeria’s financial and enterprise workforce.

Vice President Shettima, commented: “The training is a strategic national investment in capacity as infrastructure which is the human, institutional, and ethical foundations upon which inclusive growth must rest.

Shettima noted that the Aso Accord on Economic and Financial Inclusion, which the PreCEFI is mandated to implement, recognises the fact that “financial inclusion is not achieved by access alone, but by competence, trust, and capability.”

Shettima noted that the nation “cannot build a one-trillion-dollar economy on weak skills, fragmented standards, or disconnected professional ecosystems.

VP Shettima pointed out that while capacity building is financial inclusion, “without accountants who understand MSME formalisation, credit administrators who can assess risk beyond collateral, bankers who embed consumer protection, risk professionals who anticipate digital threats, and innovators who translate ideas into enterprises, inclusion remains a slogan rather than a system.”

Maintaining that the training programme must prioritise young Nigerians and women, the VP said,

“Importantly, this collaboration prioritises women and youth inclusion and digital transformation, recognising that Nigeria’s demographic dividend will only materialise if young people are equipped with relevant skills and ethical grounding for a fast-evolving digital economy.”

He charged the PreCEFI and the professional bodies not to treat the MoU as a mere document, but as a living platform for execution.

Earlier, the President of the Institute of Chartered Accountants of Nigeria (ICAN), Mallam Haruna Nma Yahaya, applauded the administration of President Bola Ahmed Tinubu for its bold economic reforms that has culminated in the flag off of the financial inclusion free training programme for 10 million women and youths in Nigeria.

He said the decision to embark on the project was prompted by visible improvements in the economy as a result of the gains of the Federal Government’s policy reforms.

Yahaya assured the Vice President of their professional support in the realisation of set objectives, describing their involvement in the project as an institutional honour.

The CEO of WAWU Africa – technical partners in the programme, Mr Emmanuel Lennox, assured of the company’s readiness to deliver on the project, particularly in providing the digital platform and overall enabling environment for its success.

The Technical Adviser to the President on Economic and Financial Inclusion, Dr Nurudeen Abubakar Zauro, emphasised why the training of 10 million Nigerians on financial inclusion had become necessary.

“Exclusion is not only by lack of access, but by limited skills, weak institutional capacity, and insufficient professional support.

Consequently, financial inclusion is not achieved by infrastructure alone; it is achieved when people and institutions are equipped to use that infrastructure responsibly, productively, and sustainably,” he said

The high point of the event was the signing of the MoU for the capacity building programme by the Federal Government and the six professional bodies.

Business

President Tinubu Approves N3.3Trn Payments Plan To Restore Reliable Electricity

Implementation has begun, with 15 power plants signing settlement agreements totalling ₦2.3 trillion.

President Bola Tinubu has approved the payment plan to finally settle the outstanding debts under the Presidential Power Sector Financial Reforms Programme.

The debt repayment plan followed the final review of the legacy debts that have beset the power sector for more than a decade.

State House press release signed by Bayo Onanuga Special Adviser to the President(Information and Strategy), said that the long-standing debts accumulated between February 2015 and March 2025.

Following verification, ₦3.3 trillion has been agreed as a full and final settlement, ensuring a fair and transparent resolution.

Implementation has begun, with 15 power plants signing settlement agreements totalling ₦2.3 trillion.

The Federal Government has already raised ₦501 billion to fund these payments.

Out of the amount, N223 billion has been disbursed, with further payments underway.

What this means for Nigerians: With payments reaching the power value chain, generation will be more stable. With power plants supported, electricity reliability will improve.

And as the sector stabilises, more investment, more jobs, and better service will follow. “This programme is not just about settling legacy debts.

It is about restoring confidence across the power sector — ensuring gas suppliers are paid, power plants can keep running, and the system begins to work more reliably”, explained Olu Arowolo-Verheijen, Special Adviser on Energy to President Tinubu.

“It is part of a broader set of reforms already underway — including better metering and service-based tariffs that link what you pay to the quality of electricity you receive.

“The government is also prioritising power supply to businesses, industries, and small enterprises — because reliable electricity is critical to creating jobs, supporting livelihoods, and growing the economy.

“The goal is simple: more reliable power for homes, stronger support for businesses, and a system that works better for all Nigerians”, she added.

President Tinubu has commended all stakeholders who supported efforts to resolve the legacy issues in the power sector.

He has also confirmed that the next phase (Series II) will begin this quarter.

Business

33 Nigerian Banks Beat CBN’s Recapialisation with ₦4.65trn Combined Capital Base

The recapitalisation programme has strengthened the capital base of Nigerian banks, reinforcing the resilience of the financial system and ensuring it is wellpositioned to support economic growth and withstand domestic and external shocks.”

•Governor of CBN, Olayemi Cardoso

The Central Bank of Nigeria (CBN) has wrapped up the banking sector recapitalisation programme it introduced two years ago (March 2024-March 31, 2026) with 33 banks successfully met the requirements deadline.

The banks raised a total of ₦4.65 trillion in new capital, according to a statement signed by Olubukola A. Akinwunmi, the Director, Banking Supervision and Hakama Sidi Ali (Mrs.), the Ag. Director, Corporate Communications.

It said that the recapialisation exercises recorded strong participation from both domestic and international investors, with 72.55% of capital sourced locally and 27.45% from international markets, reflecting sustained confidence in the Nigerian banking sector.

The statement noted that the Governor of CBN, Olayemi Cardoso said “the recapitalisation programme has strengthened the capital base of Nigerian banks, reinforcing the resilience of the financial system and ensuring it is wellpositioned to support economic growth and withstand domestic and external shocks.”

“The CBN confirms that 33 banks have met the revised minimum capital requirements established under the programme.

A limited number of institutions remain subject to ongoing regulatory and judicial processes, which are being addressed through established supervisory and legal frameworks.

“All banks remain fully operational, ensuring continued access to banking services for customers.

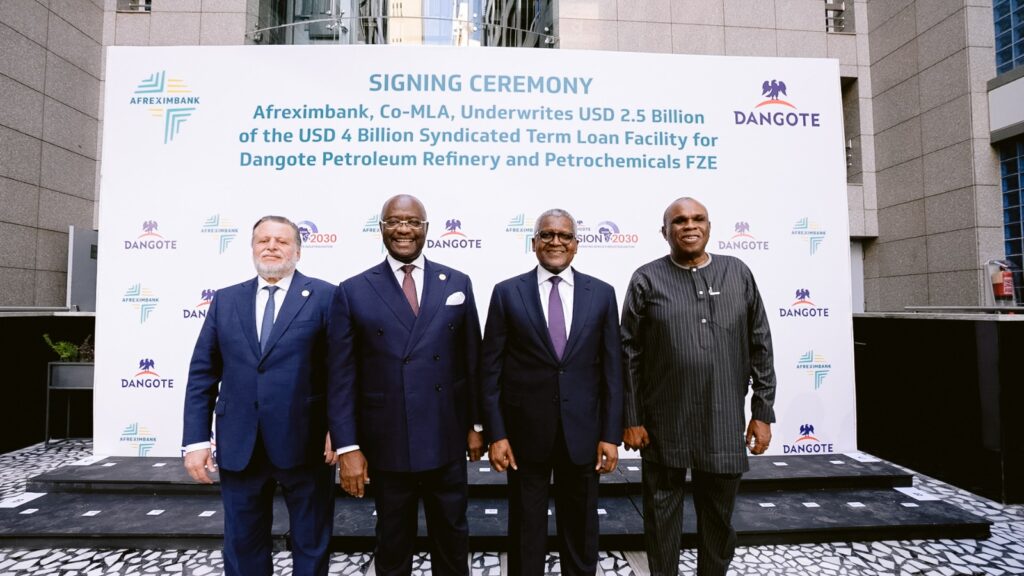

African Export-Import Bank has underwritten $2.5 billion in a $4 billion senior syndicated term loan for Dangote Petroleum Refinery and Petrochemicals, in a move aimed at strengthening the refinery’s financial position and supporting its long-term growth and expansion strategy.

The five-year facility, arranged alongside Access Bank as co-Mandated Lead Arrangers, is designed to consolidate existing debt, optimise the refinery’s capital structure and align its financing with current operational realities.

The transaction marks a significant milestone for the Dangote Refinery, Africa’s largest refining and petrochemical complex with a capacity of 650,000 barrels per day.

Afreximbank’s $2.5 billion participation represents the largest share of the syndicate, underscoring its strategic role in mobilising capital for industrial projects across the continent.

The bank said the financing aligns with its mandate to promote industrialisation, reduce reliance on imported petroleum products and deepen intra-African trade.

Since refining operations commenced in February 2024, Afreximbank has played a key role in supporting the project, including providing a $1 billion working capital facility and acting as financial adviser on the Naira-for-Crude initiative, which facilitates crude procurement and product sales in local currency.

Speaking during a strategy session in Cairo, Egypt, President and Chairman of the Board of Directors of Afreximbank, George Elombi, said the bank’s continued backing reflects confidence in indigenous African enterprises.

“We take immense pride in being the single largest provider of financing to the Dangote Group. We do so primarily because Dangote is African,” he said.

“When we invest in ourselves, we do more than create jobs and wealth or expand government revenues; we build a secure and resilient future for our continent”

Elombi disclosed that Afreximbank has committed about $15 billion to Dangote Group since 2015, highlighting the scale of its long-term partnership with the conglomerate.

President and Chief Executive of Dangote Industries Limited, Aliko Dangote, described the financing as a critical step in positioning the refinery for its next phase of expansion.

“This financing marks an important step in strengthening the financial foundation of Dangote Petroleum Refinery & Petrochemicals and positions the business for the next phase of its growth,” he said.

“We appreciate Afreximbank’s continued support and confidence in our vision to build world-class industrial capacity that serves Nigeria, Africa and global markets.”

The syndicated loan attracted strong participation from a mix of African and international financial institutions, reflecting sustained investor confidence in the refinery as a transformative industrial asset in advancing Africa’s energy security, reducing import dependence and supporting the continent’s broader industrialisation agenda.

BudgIT appoints Nigeria Country Director

Kebbi Assembly Speaker Muhammad Usman Zuru dies in Egypt

Benue Govt Confirms Total Evacuation of Benue Students From University of Jos

Tech Expert, Zuckerberg trains with UFC champions, Adesanya, Alexander

Organ Trafficking: Ekweremadu bags 10 years in UK prison

SAINT OBI: Between his marriage and his death

-

Crime3 days ago

Crime3 days agoThree Killed, One Injured in Fresh Jos Attack (Video)

-

News3 days ago

News3 days agoNigerian Army Debunks Claims of Attack on Bishop Matthew Kukah’s Residence and Sokoto Catholic Cathedral

-

News2 days ago

News2 days agoKaduna Mando Garage Explosion Not Bomb- Police

-

News2 days ago

News2 days agoAtiku hires US lobbying firm for $1.2m to boost image – Report

-

News3 days ago

News3 days agoJUST IN: Lagos Fire Service Successfully Contains Two Overnight Fire Incidents iin Lagos

-

Politics1 day ago

Politics1 day agoObidients mobilise for #OccupyINEC protest

-

Business1 day ago

Business1 day agoPresident Tinubu Approves N3.3Trn Payments Plan To Restore Reliable Electricity

-

Health2 days ago

Health2 days agoResident Doctors Set to Begin Nationwide Indefinite Strike on April 7 Over Unmet Demands